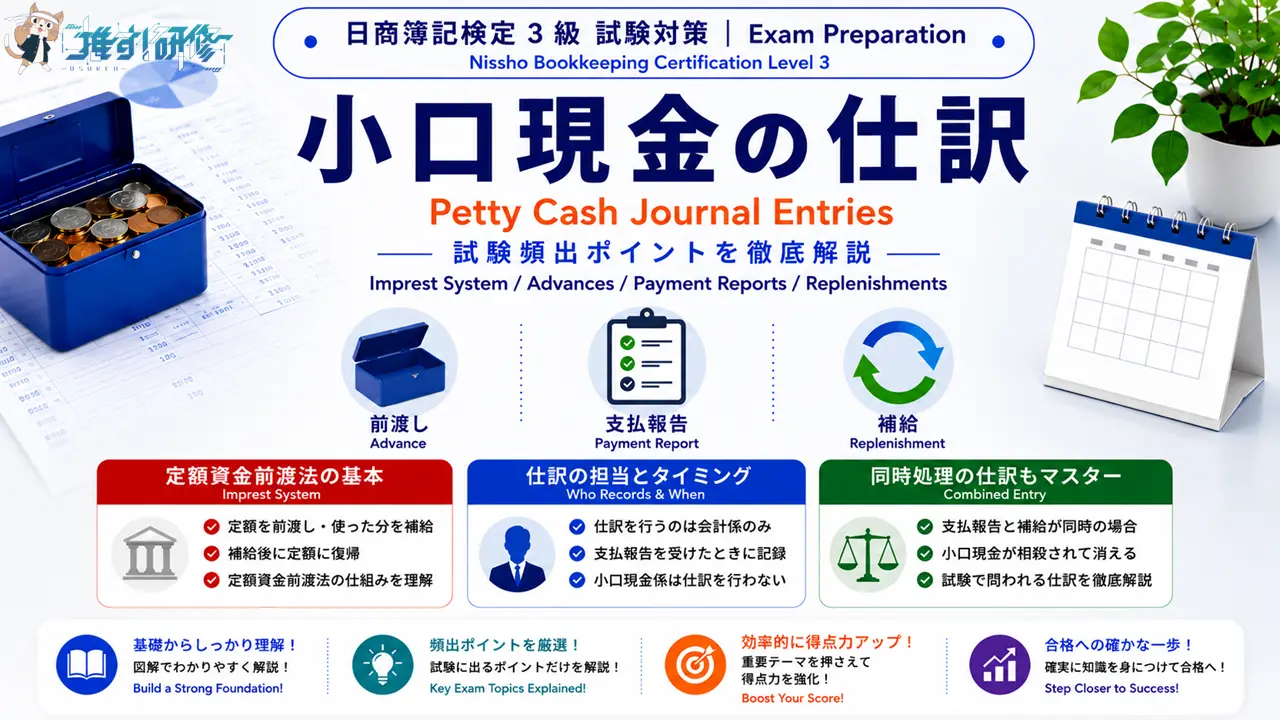

日商簿記3級|小口現金の仕訳 Nissho Bookkeeping Level 3 | Petty Cash Journal Entries

日商簿記検定3級で確実に得点したいテーマの一つが「小口現金」です。企業内で発生する細かい日常的な支出をどのように管理し記録するかを体系的に理解することが、この分野の得点力を高める鍵となります。特に「仕訳を行うタイミング」と「仕訳を行う担当者」の2点は試験で繰り返し問われる頻出論点です。本記事では、定額資金前渡法の基本的な仕組みから、前渡し・支払報告・補給それぞれの仕訳まで、試験対策に直結するポイントを体系的に解説します。

Petty cash is one of the topics where you can reliably pick up marks on the Nissho Bookkeeping Level 3 exam. The key to performing well in this area is a solid understanding of how day-to-day minor expenditures within a company are managed and recorded. Two points are tested particularly often: when journal entries are recorded, and who is responsible for recording them. This article provides a systematic explanation of the key exam points, from the fundamental structure of the imprest system through to the journal entries for advances, payment reports, and replenishments.

この記事で学べること:小口現金と定額資金前渡法の仕組み・前渡し時の仕訳・小口現金係が支払ったときの処理・支払報告を受けたときの仕訳・補給時の仕訳・支払報告と補給が同時のときの仕訳。すべて試験に出るポイントに絞っています。

What you’ll learn in this article: how petty cash and the imprest system work; the journal entry when petty cash is advanced; how payments made by the petty cashier are handled; the journal entry when a payment report is received; the journal entry for replenishment; and the combined entry when a payment report and replenishment occur on the same day. Every point is selected specifically because it appears on the exam.

目次

小口現金と定額資金前渡法の基本 Petty Cash and the Imprest System: The Basics

企業の規模が拡大すると、経理担当部門がすべての細かい支出を直接管理することが困難になります。そこで、各部署の担当者(小口現金係)にあらかじめ少額の現金を手渡しておき、日々の細かい支出に充てる仕組みが設けられます。この手渡された少額の現金を小口現金といいます。なお、会社全体の取引を帳簿に記録する担当者を会計係といいます(組織の経理担当部門がこれにあたります)。

As a company grows, it becomes impractical for the accounting department to handle every small, routine payment directly. Instead, a designated person in each department — the petty cashier — is given a small amount of cash in advance to cover day-to-day minor expenses. This pre-allocated cash is called petty cash. The staff member responsible for recording all company transactions in the books is referred to as the accountant.

定額資金前渡法とは What Is the Imprest System?

日商簿記3級では、定額資金前渡法(インプレスト・システム)と呼ばれる管理方式を前提に小口現金の処理を学びます。定額資金前渡法とは、あらかじめ決まった金額(定額)を小口現金係に前渡ししておき、一定期間ごとに使った分だけを補給することで、補給後に小口現金の残高が定額に戻る仕組みです。

In the Nissho Bookkeeping Level 3 exam, petty cash is handled using a method called the imprest system. Under this system, a fixed amount is advanced to the petty cashier in advance, and only the amount actually spent is replenished at regular intervals, so that the petty cash balance is restored to the fixed amount after each replenishment.

定額資金前渡法は、以下の4つのステップで構成されます。

The imprest system consists of the following four steps.

| ステップ / Step | 内容 / What Happens | 仕訳の担当 / Who Records the Entry |

|---|---|---|

| ①前渡し Advance | 会計係が小口現金係へ定額の現金を前渡しする The accountant advances a fixed amount of cash to the petty cashier | 会計係 Accountant |

| ②支払い Payment | 小口現金係が細かい支出を小口現金で支払う The petty cashier pays for minor expenses using petty cash | 仕訳なし No entry |

| ③報告 Report | 一定期間後、小口現金係が支出内容を会計係へ報告する After a set period, the petty cashier reports expenditures to the accountant | 会計係 Accountant |

| ④補給 Replenishment | 会計係が使った分だけ補給し、定額に戻す The accountant replenishes the amount spent, restoring the fixed balance | 会計係 Accountant |

試験対策上、最も重要なポイントは仕訳を行うのは常に会計係であり、小口現金係は仕訳を行わないという点です。また、会計係が仕訳を行うのは「支払報告を受けたとき」であり、小口現金係が支払いをした時点ではありません。この2点は試験で特に問われやすい論点です。

The most important exam point is that journal entries are always recorded by the accountant — the petty cashier never records journal entries. Furthermore, the accountant records the entry when the payment report is received, not when the petty cashier makes the payment. These two points are among the most frequently tested aspects of this topic.

小口現金の仕訳4パターン Four Journal Entry Patterns for Petty Cash

①前渡し時の仕訳(会計係) Journal Entry When Petty Cash Is Advanced

会計係が小口現金係に定額の現金を前渡しするとき、小口現金(資産)が増加し、当座預金(資産)が減少します。小口現金は資産の勘定科目です。現金の一種として位置づけられる点を押さえておきましょう。

When the accountant advances a fixed amount of cash to the petty cashier, petty cash (asset) increases and the checking account (asset) decreases. Petty cash is classified as an asset account — it should be understood as a portion of physical cash set aside for minor expenses.

例 / Example 定額資金前渡法を採用し、小切手を振り出して小口現金1,000円を小口現金係に前渡しした。

The company adopted the imprest system and advanced ¥1,000 in petty cash to the petty cashier by issuing a check.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 小口現金(資産)1,000 Petty Cash (Asset) ¥1,000 | 当座預金(資産)1,000 Checking Account / Current Account (Asset) ¥1,000 |

②支払い時の処理 Treatment When the Petty Cashier Makes a Payment

小口現金係が小口現金を使って支払いを行っても、この時点では会計係はまだ支出内容を把握していないため、仕訳は行いません。小口現金係はメモや領収書で支出内容を記録しておき、後日会計係へ報告します。

Even when the petty cashier makes payments using petty cash, the accountant does not record a journal entry at this point, because the accountant has not yet been notified of the expenditure details. The petty cashier keeps a record of all payments — using memos or receipts — and reports them to the accountant at a later date.

例 / Example 小口現金係がコピー用紙代(消耗品費)360円と宅配便代(雑費)240円を小口現金で支払った。

The petty cashier paid ¥360 for copy paper (supplies expense) and ¥240 for courier charges (miscellaneous expense) using petty cash.

| 会計係の処理 / Accountant’s Treatment |

|---|

| 仕訳なし No entry (支払報告を受けるまで会計係は仕訳を行わない / The accountant records no entry until the payment report is received) |

③支払報告を受けたときの仕訳(会計係) Journal Entry When the Payment Report Is Received

一定期間後、小口現金係から支出内容の報告を受けた会計係は、報告された費用(消耗品費・雑費など)を借方に記録し、使われた分の小口現金(資産)を貸方に記録します。小口現金は使った合計金額だけ減少します。

After a set period, when the accountant receives the payment report from the petty cashier, the accountant records the reported expenses (supplies expense, miscellaneous expense, etc.) on the debit side, and reduces petty cash (asset) on the credit side by the total amount spent.

例 / Example 小口現金係からコピー用紙代(消耗品費)360円と宅配便代(雑費)240円を支払ったという報告を受けた。

The petty cashier reported payments of ¥360 for copy paper (supplies expense) and ¥240 for courier charges (miscellaneous expense).

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 消耗品費(費用)360 Supplies Expense (Expense) ¥360 | 小口現金(資産)600 Petty Cash (Asset) ¥600 |

| 雑費(費用)240 Miscellaneous Expense (Expense) ¥240 |

報告後の小口現金残高:1,000円 − 600円 = 400円。

Petty cash balance after the report: ¥1,000 − ¥600 = ¥400.

④補給時の仕訳(会計係) Journal Entry When Petty Cash Is Replenished

定額資金前渡法では、使った分だけ小口現金を補給して定額に戻します。補給時は小口現金(資産)が増加し、当座預金(資産)が減少します。補給額は「定額 − 現在の残高」、または「前回の報告で把握した使用合計額」と一致します。

Under the imprest system, petty cash is replenished by the amount spent in order to restore the balance to the fixed amount. At the time of replenishment, petty cash (asset) increases and the checking account (asset) decreases. The replenishment amount equals the fixed amount minus the current balance, which matches the total expenditure reported in the previous report.

例 / Example 小口現金係への支払報告をもとに、使った分600円を小切手を振り出して補給した。

Based on the payment report from the petty cashier, ¥600 was replenished by issuing a check.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 小口現金(資産)600 Petty Cash (Asset) ¥600 | 当座預金(資産)600 Checking Account (Asset) ¥600 |

補給後の小口現金残高:400円 + 600円 = 1,000円(定額に復帰)。

Petty cash balance after replenishment: ¥400 + ¥600 = ¥1,000 (restored to the fixed amount).

支払報告と補給が同時のときの仕訳 Combined Entry When Report and Replenishment Occur Simultaneously

実務では、小口現金係からの支払報告と補給が同じ日に行われることがあります。このとき、③報告時の仕訳と④補給時の仕訳を合わせて1つの仕訳として処理します。2つの仕訳を合算すると、借方・貸方の両方に小口現金が登場しますが、同額の小口現金は相殺されて消え、費用の借方と当座預金の貸方だけが残ります。

In practice, the petty cashier’s payment report and the replenishment sometimes take place on the same day. In this case, the journal entries for both the payment report (③) and the replenishment (④) are combined into a single entry. When the two entries are merged, petty cash appears on both the debit and credit sides, but the equal petty cash amounts cancel each other out, leaving only the expense accounts on the debit side and the checking account on the credit side.

例 / Example 小口現金係からコピー用紙代(消耗品費)360円・宅配便代(雑費)240円の支払報告を受けると同時に、使用した合計600円を小切手を振り出して補給した。

The petty cashier reported payments of ¥360 for copy paper (supplies expense) and ¥240 for courier charges (miscellaneous expense), and at the same time ¥600 was replenished by issuing a check.

| 借方(左)/ Debit | 貸方(右)/ Credit | |

|---|---|---|

| ③報告時の仕訳 Payment report entry | 消耗品費 360 雑費 240 | 小口現金 600 |

| ④補給時の仕訳 Replenishment entry | 小口現金 600 | 当座預金 600 |

| 同時処理の仕訳 Combined entry | 消耗品費(費用)360 Supplies Expense ¥360 雑費(費用)240 Miscellaneous Expense ¥240 | 当座預金(資産)600 Checking Account ¥600 |

③と④の小口現金(600円)が相殺されて消えた結果、費用の合計600円を借方に、当座預金600円を貸方に記録するだけの仕訳になります。

Once the petty cash amounts in ③ and ④ cancel out, the combined entry simply records total expenses of ¥600 on the debit side and the checking account of ¥600 on the credit side.

試験直前チェック Key Points to Remember

小口現金の重要ポイントをまとめます。

Here is a summary of the key points on petty cash.

- 小口現金は資産の勘定科目 前渡し時に小口現金(資産)が増加し、当座預金(資産)が減少する

Petty cash is an asset account — advancing petty cash increases petty cash (asset) and decreases the checking account (asset) - 定額資金前渡法の仕組み 定額を前渡しし、使った分だけ補給することで補給後に小口現金の残高が定額に戻る方式

How the imprest system works — a fixed amount is advanced, and only the amount spent is replenished, restoring the petty cash balance to the fixed amount after each replenishment - 仕訳をするのは会計係のみ 小口現金係は仕訳を行わない。会計係は支払報告を受けたときに仕訳をする

Only the accountant records journal entries — the petty cashier never records entries; the accountant records the entry only when the payment report is received - 支払報告時の仕訳 報告された費用(消耗品費・雑費など)を借方に、使った合計額を小口現金(資産)の貸方に記録する

Journal entry at payment report — debit the reported expenses (supplies expense, miscellaneous expense, etc.) and credit petty cash (asset) for the total amount spent - 補給時の仕訳 使った分だけ補給するため、小口現金(資産)が増加し、当座預金(資産)が減少する

Journal entry at replenishment — petty cash (asset) increases and the checking account (asset) decreases by the amount replenished - 支払報告と補給が同時の場合 両仕訳の小口現金が相殺されて消える。費用の借方と当座預金の貸方だけが残る

Simultaneous report and replenishment — the petty cash entries cancel each other out, leaving only expense accounts on the debit side and the checking account on the credit side

練習問題で理解を確認しよう Practice Questions

ここまでの内容を試験形式で確認しましょう。解答と解説は各問題の直下に記載しています。

Let’s check your understanding with some exam-style practice questions. The answer and explanation for each question appear directly below it.

第1問 Question 1

次の取引に関する会計係の処理として、正しいものはどれか。

Which of the following correctly describes the accountant’s treatment for the transaction below?

【取引 / Transaction】 小口現金係が電車代(旅費交通費)150円と事務用品代(消耗品費)250円を小口現金で支払った。

The petty cashier paid ¥150 for train fare (travel expense) and ¥250 for office supplies (supplies expense) using petty cash.

- ア (旅費交通費)150・(消耗品費)250 / (小口現金)400

Debit: Travel Expense 150 / Supplies Expense 250 / Credit: Petty Cash 400 - イ 仕訳なし

No entry - ウ (小口現金)400 / (当座預金)400

Debit: Petty Cash 400 / Credit: Checking Account 400 - エ (旅費交通費)150・(消耗品費)250 / (当座預金)400

Debit: Travel Expense 150 / Supplies Expense 250 / Credit: Checking Account 400

解答:イ / Answer: イ

小口現金係が支払いを行ったとき、会計係はまだ支出内容の報告を受けていません。定額資金前渡法では、会計係が仕訳を行うのは支払報告を受けたときです。したがって、この時点での会計係の処理は「仕訳なし」となります。選択肢アは支払報告を受けたときの仕訳であり、この時点では誤りです。選択肢ウは補給時の仕訳であり、誤りです。選択肢エは報告と補給が同時のときの仕訳であり、いずれもこの場面には該当しません。

When the petty cashier makes payments, the accountant has not yet received a report of the expenditures. Under the imprest system, the accountant records a journal entry only when the payment report is received. Therefore, the correct answer is “no entry” at this point. Option ア shows the entry made upon receiving the payment report — incorrect for this stage. Option ウ shows the replenishment entry — also incorrect. Option エ shows the combined entry used when a report and replenishment occur simultaneously — none of these apply here.

第2問 Question 2

次の一連の取引について仕訳しなさい。

Record the journal entries for the following series of transactions.

- 定額資金前渡法を採用し、小切手を振り出して小口現金800円を小口現金係に前渡しした。

The imprest system was adopted and ¥800 in petty cash was advanced to the petty cashier by issuing a check. - 1週間後、小口現金係から電車代(旅費交通費)170円と郵便代(通信費)230円を支払ったという報告を受けた。

One week later, the petty cashier reported payments of ¥170 for train fare (travel expense) and ¥230 for postage (communication expense). - 本日、報告と同時に使用した400円を小切手を振り出して補給した。

Today, at the same time as the report was received, ¥400 was replenished by issuing a check.

解答 / Answer

| 借方(左)/ Debit | 貸方(右)/ Credit | |

|---|---|---|

| (1) | 小口現金(資産)800 Petty Cash (Asset) ¥800 | 当座預金(資産)800 Checking Account (Asset) ¥800 |

| (2) | 旅費交通費(費用)170 Travel Expense (Expense) ¥170 通信費(費用)230 Communication Expense (Expense) ¥230 | 小口現金(資産)400 Petty Cash (Asset) ¥400 |

| (3) | 小口現金(資産)400 Petty Cash (Asset) ¥400 | 当座預金(資産)400 Checking Account (Asset) ¥400 |

(1)定額資金前渡法により小切手を振り出して小口現金を前渡しするため、小口現金(資産)が800円増加し、当座預金(資産)が800円減少します。(2)支払報告を受けた時点で会計係が仕訳を行います。報告された費用の合計は170円+230円=400円であり、この金額だけ小口現金(資産)が減少します。(3)使用した400円分を補給するため、小口現金(資産)が400円増加し、当座預金(資産)が400円減少します。補給後の小口現金残高は400円+400円=800円(定額に復帰)となります。

(1) Since petty cash is advanced using a check under the imprest system, petty cash (asset) increases by ¥800 and the checking account (asset) decreases by ¥800. (2) The accountant records the entry upon receiving the payment report. Total reported expenses are ¥170 + ¥230 = ¥400, and petty cash (asset) decreases by this amount. (3) Since ¥400 is replenished to cover the amount spent, petty cash (asset) increases by ¥400 and the checking account (asset) decreases by ¥400. After replenishment, the petty cash balance is ¥400 + ¥400 = ¥800 (restored to the fixed amount).

第3問 Question 3

小口現金に関する次の記述のうち、誤っているものはどれか。

Which of the following statements about petty cash is incorrect?

- ア 定額資金前渡法では、小口現金係が使った金額だけを補給することで、補給後に小口現金の残高が定額に戻る。

Under the imprest system, only the amount spent by the petty cashier is replenished, restoring the petty cash balance to the fixed amount after each replenishment. - イ 小口現金係が小口現金で支払いを行ったとき、会計係はその支払いと同時に費用の仕訳を行う。

When the petty cashier makes a payment using petty cash, the accountant records an expense entry at the same time as the payment. - ウ 支払報告を受けた会計係は、報告された費用を借方に記録し、小口現金(資産)を使った分だけ貸方に記録する。

Upon receiving the payment report, the accountant debits the reported expenses and credits petty cash (asset) for the amount spent. - エ 支払報告と補給が同時に行われた場合、双方の仕訳に登場する小口現金が相殺されて消え、費用の借方と当座預金の貸方だけが残る。

When a payment report and replenishment occur simultaneously, the petty cash entries in both transactions cancel each other out, leaving only expense accounts on the debit side and the checking account on the credit side.

解答:イ / Answer: イ

選択肢イが誤りです。定額資金前渡法において、会計係が費用の仕訳を行うのは「支払報告を受けたとき」であり、小口現金係が実際に支払いを行ったときではありません。小口現金係が支払いをした時点では、会計係はその内容をまだ把握しておらず、仕訳は行いません。選択肢ア・ウ・エはいずれも正しい記述です。

Option イ is incorrect. Under the imprest system, the accountant records the expense entry when the payment report is received — not at the time the petty cashier actually makes the payment. At the time of payment, the accountant has not yet been informed of the details and therefore records no entry. Options ア, ウ, and エ are all correct statements.

- ITパスポート試験|法務の基礎知識 IT Passport Exam | Legal Affairs: Fundamentals and Key Concepts

- 危険物乙4|保安距離と保有空地の対象施設・数値基準をわかりやすく解説 Class B Group 4 Hazardous Materials Engineer | Safety Distances and Open Space Requirements Explained

この記事を書いた人

関連記事

-

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained -

日商簿記検定3級|貸付金・借入金の仕訳と利息計算 Nissho Bookkeeping Level 3 | Loans Receivable and Loans Payable: Journal Entries and Interest Calculations

-

日商簿記3級|預金と当座借越の仕訳 Nissho Bookkeeping Level 3 | Deposits and Bank Overdraft Journal Entries

-

日商簿記3級|現金の基礎知識と仕訳 Nissho Bookkeeping Level 3 | Cash: Fundamentals and Journal Entries

-

日商簿記3級|仕訳の基礎知識と借方・貸方のルール Nissho Bookkeeping Level 3 | Journal Entries: Fundamentals and Debit and Credit Rules