日商簿記3級|現金の基礎知識と仕訳 Nissho Bookkeeping Level 3 | Cash: Fundamentals and Journal Entries

日商簿記検定3級で必ず出題されるテーマの一つが「現金」です。日常生活では当たり前に使っている言葉ですが、簿記の世界では「現金」の定義が少し異なります。その違いを正確に押さえておくことが、この分野の問題を確実に得点するための鍵です。本記事では、簿記上の現金の定義から現金過不足の処理まで、試験に直結するポイントを一つひとつ整理します。

Cash is one of the frequently tested topics on the Nissho Bookkeeping Level 3 exam. The word itself is familiar in everyday life, but in bookkeeping, “cash” carries a somewhat different definition — and understanding that difference precisely is the key to scoring reliably on this topic. This article systematically works through the key exam points, from the bookkeeping definition of cash to handling cash shortages and overages.

この記事で学べること:簿記上の現金の意味(通貨代用証券)・他人振出小切手と自己振出小切手の違い・現金過不足の3つの処理パターン。すべて試験に出るポイントに絞っています。

What you’ll learn in this article: the bookkeeping definition of cash (items treated as cash); the difference between checks drawn by others and checks drawn by your own company; and the three patterns for handling cash shortages and overages. Every point is chosen specifically because it appears on the exam.

目次

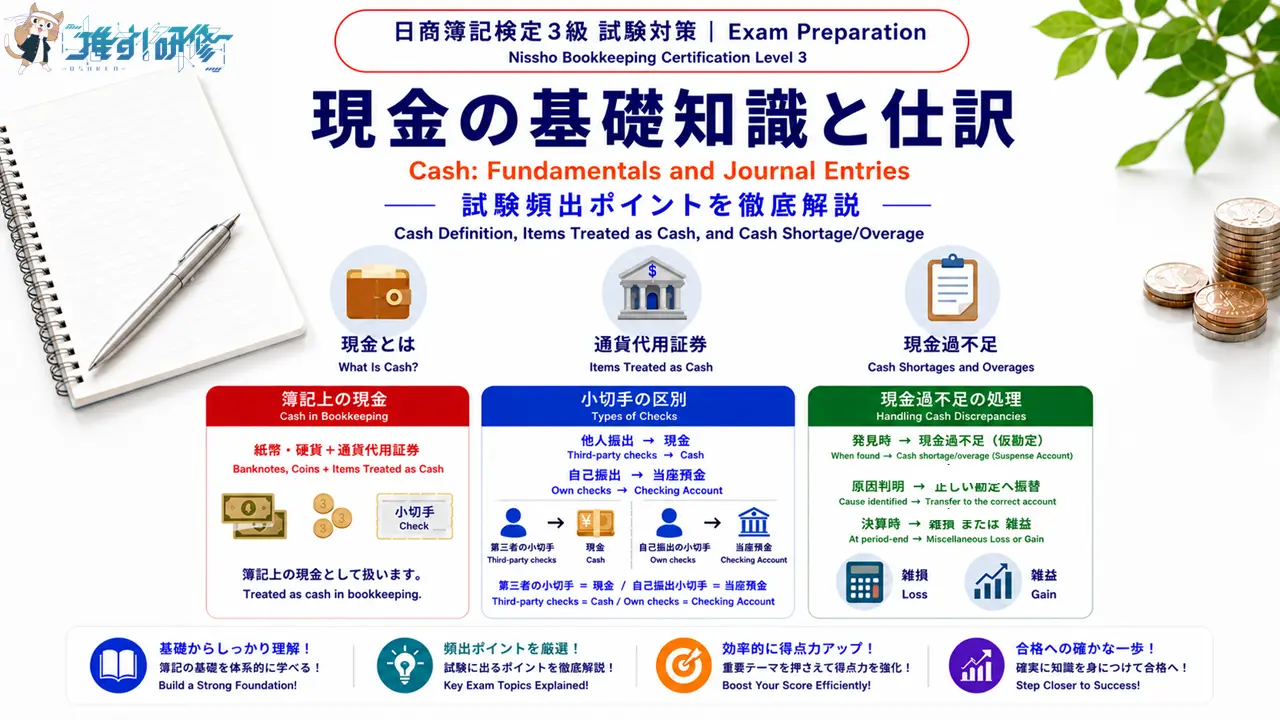

簿記上の「現金」とは / What Is “Cash” in Bookkeeping?

日常生活では「現金=お札や硬貨」ですよね。しかし簿記では、現金とは、紙幣・硬貨だけでなく、銀行などですぐに現金に換えられるものも含むと定義されています。こうした「すぐに現金化できる証券類」をまとめて「通貨代用証券(つうかだいようしょうけん)」と呼びます。

In everyday life, cash means bills and coins. In bookkeeping, however, cash includes not only banknotes and coins, but also anything that can be immediately exchanged for cash at a bank. These items are grouped together under the term “items treated as cash” (通貨代用証券).

簿記上の現金に含まれる代表的なものを確認しましょう。まず、紙幣・硬貨(日本円・外貨)はそのまま現金です。次に、他人振出小切手(たにんふりだしこぎって)とは、取引先など他の人や会社が振り出した小切手のことです。銀行の窓口ですぐに現金化できるため、現金として扱います。また、送金小切手(送金手段として銀行が振り出す小切手)や普通(郵便)為替証書(送金手段として郵便局で取り扱うもの)も、すぐに現金化できるため現金として扱います。

Here are the main items that count as cash in bookkeeping. First, banknotes and coins (Japanese yen and foreign currency) are cash as you would expect. Next, checks drawn by others (他人振出小切手) are checks issued by a business partner or another company — they can be cashed immediately at a bank counter and are therefore treated as cash. Remittance checks (checks issued by a bank as a means of remittance) and ordinary (postal) money orders (handled at post offices as a means of remittance) can also be cashed right away, so they are also treated as cash.

重要ポイント / Key Point

「自己振出小切手(じこふりだしこぎって)」に注意! これは自分の会社が振り出した小切手のことです。この小切手が手元に戻ってきたとき、現金として記録するのではなく、「当座預金の増加」として処理します。現金として扱われるのは、あくまで他人が振り出した小切手だけです。試験でよく問われる区別なので、しっかり覚えておきましょう。

Watch out for checks drawn by your own company (自己振出小切手)! When a check that your own company originally issued comes back to you, it is not recorded as cash — instead, it is recorded as an increase in the checking account. Only checks drawn by someone else are treated as cash. This is a distinction the exam tests frequently, so make sure you remember it.

現金過不足 / Cash Shortages and Overages

金庫の中のお金を実際に数えたとき、帳簿上の残高と一致しないことがあります。これを現金過不足(げんきんかふそく)といいます。「帳簿より現金が少ない=不足」「帳簿より現金が多い=過剰」です。現金過不足が生じたときは、まず帳簿を実際の残高に合わせ、原因が分かったら正しい勘定科目に振り替えます。

Sometimes when you physically count the cash in the safe or register, the amount does not match the book balance. This is called a cash shortage or overage (現金過不足). If the actual amount is less than the book balance, it is a shortage; if it is more, it is an overage. When this happens, the book balance is first corrected to match the actual amount, and once the cause is identified, the entry is transferred to the correct account title.

現金過不足の処理手順 / How to Handle Cash Shortages and Overages

現金過不足の処理は、次の3つのパターンで理解しましょう。

There are three patterns to understand when handling cash shortages and overages.

パターン1:発見したとき。実際の残高と帳簿残高の差額を「現金過不足(仮の勘定科目)」として記録し、帳簿を実際の残高に合わせます。現金が帳簿より少ない(不足)場合は「現金過不足」を借方に、現金が帳簿より多い(過剰)場合は「現金過不足」を貸方に記録します。

Pattern 1: When the difference is discovered. The difference between the actual balance and the book balance is recorded using “Cash Shortage/Overage” as a temporary account, and the book balance is corrected to match the actual amount. If cash is less than the book balance (shortage), record “Cash Shortage/Overage” on the debit side; if cash is more (overage), record it on the credit side.

例(不足)/ Example (shortage) 帳簿残高60,000円のところ、実際の現金残高が55,000円だった(不足5,000円)。

The book balance was ¥60,000, but the actual cash counted was ¥55,000 (shortage of ¥5,000).

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 現金過不足 5,000 Cash Shortage/Overage ¥5,000 | 現金(資産) 5,000 Cash (Asset) ¥5,000 |

例(過剰)/ Example (overage) 帳簿残高40,000円のところ、実際の現金残高が43,000円だった(過剰3,000円)。

The book balance was ¥40,000, but the actual cash counted was ¥43,000 (overage of ¥3,000).

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 現金(資産) 3,000 Cash (Asset) ¥3,000 | 現金過不足 3,000 Cash Shortage/Overage ¥3,000 |

パターン2:原因が分かったとき。原因が判明したら、「現金過不足」を正しい勘定科目に振り替えます。たとえば、現金不足の原因が「通信費の記帳漏れ」であれば「通信費(費用)」に振り替えます。

Pattern 2: When the cause is identified. Once the cause is known, the “Cash Shortage/Overage” entry is transferred to the correct account title. For example, if the shortage was caused by a communication expense that was never recorded, it is transferred to “Communication Expenses” (費用).

例 / Example パターン1(不足)で記録した5,000円のうち、3,000円は通信費の記帳漏れと判明した。

Of the ¥5,000 shortage recorded in Pattern 1, ¥3,000 was found to be an unrecorded communication expense.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 通信費(費用) 3,000 Communication Expenses (Expense) ¥3,000 | 現金過不足 3,000 Cash Shortage/Overage ¥3,000 |

パターン3:決算日になっても原因が分からないとき。現金過不足は「仮の勘定科目」のため、決算日(期末)まで帳簿に残しておくことはできません。決算日になっても原因が不明な場合は、不足額を「雑損(ざっそん)」(費用)、過剰額を「雑益(ざつえき)」(収益)として処理して帳簿を締めます。

Pattern 3: When the cause is still unknown at year-end. Because “Cash Shortage/Overage” is a temporary account, it cannot remain in the books at year-end. If the cause is still unknown at the closing date, any remaining shortage is recorded as “Miscellaneous Loss” (雑損 — an expense), and any remaining overage is recorded as “Miscellaneous Gain” (雑益 — revenue).

例 / Example パターン2で処理した後も、現金過不足の残額2,000円(不足)の原因が決算日まで判明しなかった。

After the entry in Pattern 2, the remaining ¥2,000 shortage in Cash Shortage/Overage had no identified cause by year-end.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 雑損(費用) 2,000 Miscellaneous Loss (Expense) ¥2,000 | 現金過不足 2,000 Cash Shortage/Overage ¥2,000 |

試験直前チェック Key Points to Remember

日商簿記3級における現金の重要ポイントをまとめます。

Here is a summary of the key points on cash for the Nissho Bookkeeping Level 3 exam.

- 簿記上の現金 紙幣・硬貨だけでなく、他人振出小切手・送金小切手・普通(郵便)為替証書(通貨代用証券)も含む。自己振出小切手は現金ではなく当座預金として処理する

Cash in bookkeeping — Includes not only banknotes and coins, but also checks drawn by others, remittance checks, and ordinary (postal) money orders (items treated as cash). Checks drawn by your own company are recorded as a checking account entry, not as cash - 現金過不足の処理(3パターン) ①発見時:「現金過不足(仮勘定)」で記録し帳簿を修正 ②原因判明時:正しい勘定科目に振り替える ③決算時・原因不明:不足は雑損(費用)、過剰は雑益(収益)として処理する

Handling cash shortages and overages (3 patterns) — ① When discovered: record as “Cash Shortage/Overage” (temporary) and correct the books ② When cause is identified: transfer to the correct account ③ At year-end if cause is unknown: shortage → Miscellaneous Loss (expense); overage → Miscellaneous Gain (revenue)

練習問題で理解を確認しよう Practice Questions

ここまでの内容を試験形式で確認しましょう。解答と解説は各問題の直下に記載しています。

Let’s check your understanding with some exam-style practice questions. The answer and explanation for each question appear directly below it.

第1問 Question 1

簿記上の「現金」として取り扱われるものとして、適切なものはどれか。

Which of the following is correctly treated as “cash” in bookkeeping?

- 自社が取引先に振り出した小切手

A check drawn by your own company and issued to a business partner - 満期日が到来していない定期預金証書

A time deposit certificate that has not yet reached its maturity date - 取引先から受け取った他人振出小切手

A check drawn by another party, received from a business partner - 郵便切手

A postage stamp

解答:3 / Answer: 3

他人振出小切手は銀行の窓口ですぐに現金化できるため、簿記上の現金(通貨代用証券)として扱います。選択肢1の自社振出小切手は、手元に戻ってきたとき現金ではなく当座預金として処理します。選択肢2の満期未到来の定期預金証書はすぐに現金化できないため「定期預金(資産)」として処理し、現金には含みません。選択肢4の郵便切手は銀行で現金化できないため、簿記上の現金には含まれません。切手はまだ使っていない場合は「貯蔵品(資産)」、使用した時点で「通信費(費用)」として処理します。

A check drawn by another party can be cashed immediately at a bank counter, so it is treated as bookkeeping cash (an item treated as cash). Option 1: a check drawn by your own company is recorded as a checking account entry — not as cash — when it is returned to you. Option 2: a time deposit certificate that has not yet matured cannot be cashed immediately, so it is recorded as “Time Deposit” (an asset) and is not included in cash. Option 4: a postage stamp cannot be cashed at a bank, so it is not included in bookkeeping cash. Unused stamps are recorded as “Supplies on Hand” (貯蔵品 — an asset); once used, they are recorded as “Communication Expenses” (通信費 — an expense).

第2問 Question 2

次の一連の取引について仕訳しなさい。

Record the journal entries for the following series of transactions.

- 金庫を調べたところ、現金の実際有高は90,000円であるが、帳簿残高は96,000円であった。

Upon counting the cash in the safe, the actual balance was ¥90,000, but the book balance was ¥96,000. - (1)の現金過不足の原因を調べたところ、4,000円については通信費の支払いが記帳漏れであることが判明した。

Investigating the cause of the shortage in (1), it was found that ¥4,000 was an unrecorded communication expense payment. - 本日決算日につき、(1)で生じた現金過不足のうち原因不明の残額について雑損または雑益で処理する。

Today is the closing date. The remaining unexplained amount from the shortage in (1) is to be recorded as Miscellaneous Loss or Miscellaneous Gain.

解答 / Answer

| 借方(左)/ Debit | 貸方(右)/ Credit | |

|---|---|---|

| (1) | 現金過不足 6,000 Cash Shortage/Overage ¥6,000 | 現金(資産) 6,000 Cash (Asset) ¥6,000 |

| (2) | 通信費(費用) 4,000 Communication Expenses ¥4,000 | 現金過不足 4,000 Cash Shortage/Overage ¥4,000 |

| (3) | 雑損(費用) 2,000 Miscellaneous Loss ¥2,000 | 現金過不足 2,000 Cash Shortage/Overage ¥2,000 |

(1)帳簿残高(96,000円)が実際有高(90,000円)より6,000円多い「現金不足」の状態です。帳簿を実際有高に合わせるため、現金(資産)を6,000円減らします。現金(資産)の減少は貸方なので、借方:現金過不足 6,000 / 貸方:現金 6,000 となります。(2)原因が判明した4,000円分を、正しい勘定科目「通信費(費用)」に振り替えます。(3)決算日になっても残る原因不明の2,000円(6,000円 − 4,000円)は不足なので、「雑損(費用)」として処理します。

(1) The book balance (¥96,000) exceeds the actual balance (¥90,000) by ¥6,000 — a cash shortage. To bring the books in line with the actual amount, cash (an asset) must be decreased by ¥6,000. A decrease in an asset goes on the credit side, so the entry is: Debit: Cash Shortage/Overage 6,000 / Credit: Cash 6,000. (2) The ¥4,000 with an identified cause is transferred to the correct account, “Communication Expenses.” (3) The remaining ¥2,000 (¥6,000 − ¥4,000) with no identified cause at year-end is a shortage, so it is recorded as “Miscellaneous Loss” (an expense).

第3問 Question 3

次の取引の仕訳として、適切なものはどれか。

Which of the following is the correct journal entry for the transaction below?

【取引 / Transaction】 現金の実際残高を確認したところ、帳簿残高150,000円に対して実際残高は154,000円であった。差額の原因は不明である。

Upon counting the cash on hand, the actual balance was ¥154,000 against a book balance of ¥150,000. The cause of the difference is unknown.

- (借方)現金 4,000 / (貸方)雑益 4,000

Debit: Cash 4,000 / Credit: Miscellaneous Gain 4,000 - (借方)現金過不足 4,000 / (貸方)現金 4,000

Debit: Cash Shortage/Overage 4,000 / Credit: Cash 4,000 - (借方)現金 4,000 / (貸方)現金過不足 4,000

Debit: Cash 4,000 / Credit: Cash Shortage/Overage 4,000 - (借方)雑損 4,000 / (貸方)現金過不足 4,000

Debit: Miscellaneous Loss 4,000 / Credit: Cash Shortage/Overage 4,000

解答:3 / Answer: 3

実際残高(154,000円)が帳簿残高(150,000円)より4,000円多い「現金過剰」の状態です。帳簿を実際残高に合わせるには、現金を4,000円増やす必要があります。現金(資産)の増加は借方なので、「借方:現金 4,000 / 貸方:現金過不足 4,000」が正解です。選択肢1は、原因がまだ不明な段階で雑益を使っており誤りです(雑益を使うのは決算時)。選択肢2は現金が減少する仕訳であり、今回の「過剰」の場合には誤りです。選択肢4は「決算時・原因不明・不足」のケースの仕訳であり、今回は「過剰・発見時」のケースなので誤りです。

The actual balance (¥154,000) is ¥4,000 more than the book balance (¥150,000) — a cash overage. To bring the book balance in line with the actual amount, cash must be increased by ¥4,000. An increase in cash (an asset) goes on the debit side, so the correct entry is: Debit: Cash 4,000 / Credit: Cash Shortage/Overage 4,000. Option 1 is incorrect because Miscellaneous Gain is used before the cause is known — it is only used at year-end. Option 2 is a cash-decrease entry and is incorrect for an overage. Option 4 applies to a year-end, cause-unknown shortage — the situation here is an overage discovered during the period, so it does not apply.

- 日商簿記3級|仕訳の基礎知識と借方・貸方のルール Nissho Bookkeeping Level 3 | Journal Entries: Fundamentals and Debit and Credit Rules

- ITパスポート試験|開発技術の基礎知識とソフトウェア開発モデル IT Passport Exam | Development Technology: Fundamentals and Software Development Models

この記事を書いた人

関連記事

-

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained -

日商簿記検定3級|貸付金・借入金の仕訳と利息計算 Nissho Bookkeeping Level 3 | Loans Receivable and Loans Payable: Journal Entries and Interest Calculations

-

日商簿記3級|小口現金の仕訳 Nissho Bookkeeping Level 3 | Petty Cash Journal Entries

-

日商簿記3級|預金と当座借越の仕訳 Nissho Bookkeeping Level 3 | Deposits and Bank Overdraft Journal Entries

-

日商簿記3級|仕訳の基礎知識と借方・貸方のルール Nissho Bookkeeping Level 3 | Journal Entries: Fundamentals and Debit and Credit Rules