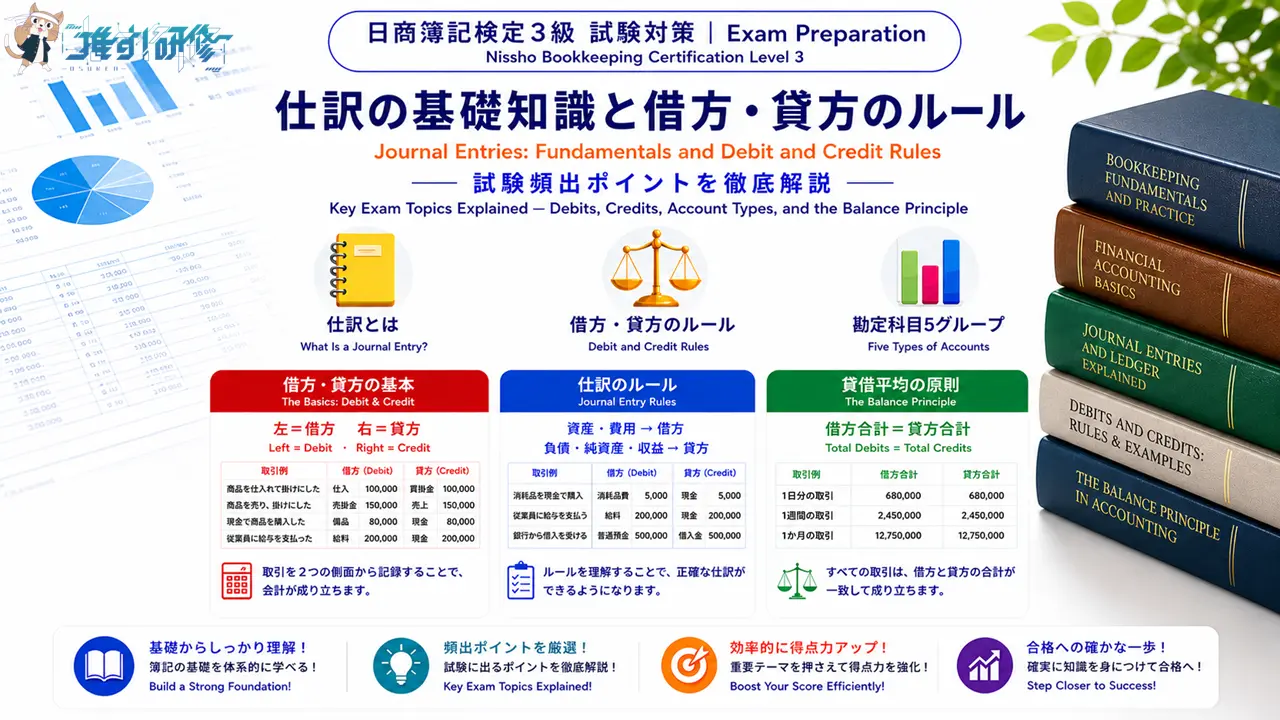

日商簿記3級|仕訳の基礎知識と借方・貸方のルール Nissho Bookkeeping Level 3 | Journal Entries: Fundamentals and Debit and Credit Rules

日商簿記検定3級の合否を分けるといっても過言ではないのが「仕訳」です。試験のあらゆる場面で仕訳の知識が求められるため、借方・貸方のルールをしっかり身につけることが合格への最短ルートとなります。本記事では、仕訳の基本的な考え方から勘定科目の5グループ・貸借平均の原則まで、順を追って丁寧に整理していきます。

Journal entries are at the heart of the Nissho Bookkeeping Level 3 exam — they come up in virtually every section, and a solid grasp of debit and credit rules is the most direct route to passing. This article carefully works through the fundamentals of journal entries in a logical sequence, from the basic concept of debits and credits to the five account types and the principle that debits equal credits.

目次

仕訳とは What Is a Journal Entry?

企業では毎日、商品を売ったり、代金を受け取ったり、経費を支払ったりといった「お金に関するできごと」が発生します。簿記では、こうしたできごとのことを取引(とりひき)と呼びます。

Every day, businesses engage in money-related events — selling goods, receiving payments, paying expenses, and so on. In bookkeeping, these events are called transactions.

仕訳(しわけ)とは、取引が発生するたびに、その内容を「借方(かりかた)」と「貸方(かしかた)」の2つの側に分けて記録する作業のことです。仕訳は、帳簿(ちょうぼ)に記録するための基本的な手順であり、すべての会計処理の出発点です。「日記に毎日の出来事を書き留めるように、取引を毎回記録していく」とイメージすると覚えやすいです。

A journal entry is the process of recording each transaction by splitting it into two sides: the debit side (借方) on the left, and the credit side (貸方) on the right. A journal entry is the fundamental step for recording in the account books and is the starting point for all accounting processes. A helpful way to picture it: just as you write down what happened each day in a diary, you record every transaction as it occurs.

借方・貸方とは What Are Debit and Credit?

「借方」「貸方」という言葉を初めて聞いたとき、「借りる」「貸す」という日本語の意味と結びつけようとして混乱する方が多いです。これらの用語は、明治期に西洋式簿記が日本に翻訳・導入される中で定着した用語とされており、歴史的にはかすかな関連がありますが、現在の簿記では「借方」は仕訳の左側、「貸方」は仕訳の右側を示す「場所の名前」として使われており、「借りる・貸す」という意味はなくなっています。左側に何を書くか、右側に何を書くかは、後述するルールによって決まります。

When people first encounter the words “debit” (借方) and “credit” (貸方), many try to connect them to their literal Japanese meanings of “borrowing” and “lending” — and become confused. The Japanese terms for debit and credit became established during the Meiji era as Western-style bookkeeping was translated and introduced into Japan, and while there is a faint historical connection to borrowing and lending, in modern bookkeeping “debit” simply refers to the left side of a journal entry and “credit” to the right side — the sense of “borrowing” or “lending” has fallen away entirely. What goes on the left and what goes on the right is determined by the rules explained below.

仕訳は次のような形式で書きます。

A journal entry is written in the following format.

| 借方(左側)/ Debit (Left) | 貸方(右側)/ Credit (Right) |

|---|---|

| 勘定科目 金額 Account title Amount | 勘定科目 金額 Account title Amount |

仕訳の大原則:借方の合計金額と貸方の合計金額は、必ず一致します。これを「貸借平均の原則」といいます。左右が常にバランスしていることが、簿記の基本中の基本です。

The fundamental rule of journal entries: the total amount on the debit side must always equal the total amount on the credit side. This is called the “principle of debit-credit balance.” The fact that the left and right sides always balance is one of the most fundamental concepts in bookkeeping.

勘定科目の5つのグループ The Five Groups of Account Titles

仕訳を書くときは、取引の内容を「勘定科目(かんじょうかもく)」という名前で分類します。勘定科目とは、取引の内容を種類ごとに整理するための名前(ラベル)のことです。「現金」「売掛金」「借入金」「売上」「給料」などがその例です。

When writing a journal entry, the content of the transaction is classified using names called “account titles” (勘定科目). An account title is a label used to organize transactions by type. Examples include “Cash” (現金), “Accounts Receivable” (売掛金), “Loans Payable” (借入金), “Sales” (売上), and “Salary Expense” (給料).

勘定科目はすべて、次の5つのグループのいずれかに属しています。このグループ分けを理解することが、仕訳のルールを覚えるための最重要ステップです。

Every account title belongs to one of the following five groups. Understanding this grouping is the single most important step toward learning the rules of journal entries.

①資産(しさん)とは、企業が所有する財産のことです。現金・預金・売掛金・建物・備品などがあります。②負債(ふさい)とは、企業が将来返済しなければならない義務(借金)のことです。借入金・買掛金・未払金などがあります。③純資産(じゅんしさん)とは、資産から負債を差し引いた残り(自分のもの)のことです。資本金・繰越利益剰余金などがあります。④収益(しゅうえき)とは、企業が稼いだ収入のことです。売上・受取利息・受取手数料などがあります。⑤費用(ひよう)とは、企業が事業のために使ったお金のことです。仕入・給料・家賃・水道光熱費などがあります。

① Assets (資産) are the property owned by a business — cash, bank deposits, accounts receivable, buildings, equipment, and so on. ② Liabilities (負債) are obligations the business must repay in the future — borrowings, accounts payable, accrued expenses, and so on. ③ Equity / Net Assets (純資産) are what remains after subtracting liabilities from assets — capital stock, retained earnings, and so on. ④ Revenue (収益) is income earned by the business — sales, interest received, fees received, and so on. ⑤ Expenses (費用) are money spent to run the business — purchases, salaries, rent, utilities, and so on.

貸借対照表と損益計算書の関係 The Relationship Between the Balance Sheet and the Income Statement

5つのグループは、財務諸表(ざいむしょひょう)と次のように対応しています。資産・負債・純資産の3グループは貸借対照表(バランスシート)に記載されます。貸借対照表は「ある時点での企業の財産と借金の状態」を表す書類です。一方、収益・費用の2グループは損益計算書(そんえきけいさんしょ)に記載されます。損益計算書は「ある期間で企業がどれだけ儲けたか(損したか)」を表す書類です。

The five groups correspond to financial statements as follows. The three groups of assets, liabilities, and equity are reported on the balance sheet (貸借対照表). The balance sheet shows the state of a company’s assets and debts at a specific point in time. The two groups of revenue and expenses are reported on the income statement (損益計算書). The income statement shows how much profit (or loss) the company generated over a given period.

仕訳のルール The Rules of Journal Entries

いよいよ仕訳の核心です。5つのグループそれぞれに「増えたとき・減ったとき、どちらに書くか」というルールがあります。このルールを覚えることが、仕訳の第一歩です。試験では、取引の内容を読んで「何が増えて、何が減ったか」を判断し、このルールに従って左右に振り分ける問題が出ます。

Now we come to the heart of journal entries. Each of the five groups has a rule for “which side to write on when it increases, and which side when it decreases.” Memorizing these rules is the first step in mastering journal entries. The exam presents a transaction, asks you to determine “what increased and what decreased,” and requires you to assign each item to the correct side following these rules.

| グループ / Group | 借方(左)に記録する場合 When to Record on Debit (Left) | 貸方(右)に記録する場合 When to Record on Credit (Right) |

|---|---|---|

| 資産 / Assets | ✔ 増加 / Increase | ✔ 減少 / Decrease |

| 負債 / Liabilities | ✔ 減少 / Decrease | ✔ 増加 / Increase |

| 純資産 / Equity | ✔ 減少 / Decrease | ✔ 増加 / Increase |

| 収益 / Revenue | ✔ 消滅 / Elimination | ✔ 発生 / Occurrence |

| 費用 / Expenses | ✔ 発生 / Occurrence | ✔ 消滅 / Elimination |

なお、日本の簿記教育では、収益・費用については単なる「増加・減少」ではなく、「発生・消滅」と表現することがあります。これは収益と費用が会計期間の中で発生し、決算を経て消滅するという概念を反映したものです。

In Japanese bookkeeping education, revenue and expenses are often described as “occurring” (発生) and “disappearing” (消滅) over an accounting period, rather than simply increasing or decreasing.

重要ポイント / Key Point

資産が増えたら借方(左)、資産が減ったら貸方(右)です。負債・純資産・収益はその逆で、増えたら貸方(右)、減ったら借方(左)です。費用は資産と同じく、発生したら借方(左)です。「資産と費用は借方、負債・純資産・収益は貸方」と大きくとらえると覚えやすいです。

When assets increase, record on the debit (left) side; when assets decrease, record on the credit (right) side. Liabilities, equity, and revenue are the opposite — increases go on the credit (right) side, decreases on the debit (left) side. Expenses follow the same pattern as assets: when they occur, record on the debit (left) side. A useful shorthand: “assets and expenses go debit; liabilities, equity, and revenue go credit.”

仕訳の具体例 Worked Examples

ルールを具体的な取引に当てはめて確認しましょう。仕訳は次の手順で考えます。①取引に登場する勘定科目を特定する、②各勘定科目が5つのグループのどれに属するか確認する、③増えたか・減ったかを判断する、④ルール表に従って借方・貸方に振り分ける。

Let’s apply the rules to specific transactions. Use the following steps: ① Identify the account titles in the transaction. ② Determine which of the five groups each belongs to. ③ Decide whether each item increased or decreased. ④ Assign to debit or credit following the rule table.

例1 / Example 1 商品を10,000円で現金販売した。

Sold goods for ¥10,000 cash.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 現金(資産)10,000 Cash (Asset) ¥10,000 | 売上(収益)10,000 Sales (Revenue) ¥10,000 |

現金(資産)が10,000円増えた → 借方。売上(収益)が10,000円発生した → 貸方。

Cash (Asset) increased by ¥10,000 → Debit. Sales (Revenue) of ¥10,000 occurred → Credit.

例2 / Example 2 事務所の家賃30,000円を現金で支払った。

Paid office rent of ¥30,000 in cash.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 支払家賃(費用)30,000 Rent Expense (Expense) ¥30,000 | 現金(資産)30,000 Cash (Asset) ¥30,000 |

支払家賃(費用)が30,000円発生した → 借方。現金(資産)が30,000円減った → 貸方。

Rent Expense (Expense) of ¥30,000 occurred → Debit. Cash (Asset) decreased by ¥30,000 → Credit.

例3 / Example 3 銀行から100,000円を借り入れ、当座預金に預け入れた。

Borrowed ¥100,000 from a bank and deposited it into a checking account.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 当座預金(資産)100,000 Checking Account (Asset) ¥100,000 | 借入金(負債)100,000 Loans Payable (Liability) ¥100,000 |

当座預金(資産)が100,000円増えた → 借方。借入金(負債)が100,000円増えた → 貸方。

Checking Account (Asset) increased by ¥100,000 → Debit. Loans Payable (Liability) increased by ¥100,000 → Credit.

主な勘定科目の一覧 Key Account Titles by Group

試験でよく登場する主要な勘定科目をグループ別に整理します。初めて目にする科目も、「これは資産か?費用か?」というグループを確認することで、仕訳のルールをすぐに適用できます。

Below is a summary of the key account titles frequently seen in the exam, organized by group. Even when encountering an unfamiliar title, confirming “is this an asset? an expense?” allows you to apply the rules immediately.

| グループ / Group | 主な勘定科目 / Key Account Titles |

|---|---|

| 資産 / Assets | 現金、当座預金、普通預金、売掛金、受取手形、商品、建物、備品、車両運搬具 Cash, Checking Account, Ordinary Deposit, Accounts Receivable, Notes Receivable, Merchandise, Building, Equipment, Vehicles |

| 負債 / Liabilities | 買掛金、支払手形、借入金、未払金、前受金 Accounts Payable, Notes Payable, Loans Payable, Accrued Expenses, Advances Received |

| 純資産 / Equity | 資本金、繰越利益剰余金 Capital Stock, Retained Earnings |

| 収益 / Revenue | 売上、受取利息、受取手数料、受取家賃 Sales, Interest Received, Fees Received, Rent Received |

| 費用 / Expenses | 仕入、給料、支払家賃、水道光熱費、支払利息、旅費交通費、通信費、消耗品費 Purchases, Salaries, Rent Expense, Utilities, Interest Expense, Travel Expenses, Communication Expenses, Supplies Expense |

試験直前チェック Key Points to Remember

日商簿記3級における仕訳の重要ポイントをまとめます。

Here is a summary of the key points on journal entries for the Nissho Bookkeeping Level 3 exam.

- 仕訳とは 取引を借方(左)と貸方(右)の2つに分けて記録する作業。借方・貸方は「場所の名前」であり、「借りる・貸す」とは無関係

What a journal entry is — The act of recording a transaction by splitting it into debit (left) and credit (right). Debit and credit are simply position names, unrelated to borrowing or lending - 貸借平均の原則 借方合計=貸方合計。仕訳の左右は必ず金額が一致する

Principle of debit-credit balance — Total debits = total credits. The left and right sides of a journal entry must always equal each other - 5つのグループ 資産・負債・純資産(→貸借対照表)、収益・費用(→損益計算書)

Five groups — Assets, liabilities, and equity (→ balance sheet); revenue and expenses (→ income statement) - 仕訳のルール 資産・費用は増加で借方。負債・純資産・収益は増加で貸方。減少・消滅は逆側に記録する

Journal entry rules — Assets and expenses go debit when they increase. Liabilities, equity, and revenue go credit when they increase. Decreases and settlements are recorded on the opposite side - 手順 ①勘定科目を特定 → ②グループを確認 → ③増減を判断 → ④ルールに従って左右に振り分ける

Steps — ① Identify account titles → ② Confirm the group → ③ Determine increase or decrease → ④ Assign to debit or credit following the rules

練習問題で理解を確認しよう Practice Questions

ここまでの内容を試験形式で確認しましょう。解答と解説は各問題の直下に記載しています。

Let’s test what you’ve learned with some exam-style practice questions. The answer and explanation for each question appear directly below it.

第1問 Question 1

仕訳の基本的な考え方について、次の記述のうち適切なものはどれか。

Regarding the fundamental concept of journal entries, which of the following statements is correct?

- 借方とは「お金を借りた」ことを記録する側であり、貸方とは「お金を貸した」ことを記録する側である。

“Debit” is the side for recording money borrowed, and “credit” is the side for recording money lent. - 仕訳では、借方の合計金額と貸方の合計金額は必ず一致する。

In a journal entry, the total amount on the debit side must always equal the total amount on the credit side. - 資産が増加したときは、貸方(右側)に記録する。

When an asset increases, it is recorded on the credit (right) side. - 収益が発生したときは、借方(左側)に記録する。

When revenue occurs, it is recorded on the debit (left) side.

解答:2 / Answer: 2

選択肢2は「貸借平均の原則」の正しい説明です。仕訳では借方(左)と貸方(右)の金額の合計が必ず一致します。選択肢1は誤りで、借方・貸方は「場所の名前」であり、「借りる・貸す」という意味とは無関係です。選択肢3は誤りで、資産が増加したときは借方(左側)に記録します。選択肢4は誤りで、収益が発生したときは貸方(右側)に記録します。

Option 2 correctly describes the “principle of debit-credit balance.” In a journal entry, the total amounts on the debit (left) and credit (right) sides must always match. Option 1 is incorrect: debit and credit are simply position names, unrelated to “borrowing” or “lending.” Option 3 is incorrect: when an asset increases, it is recorded on the debit (left) side. Option 4 is incorrect: when revenue occurs, it is recorded on the credit (right) side.

第2問 Question 2

次の取引の仕訳として、適切なものはどれか。

Which of the following is the correct journal entry for the transaction below?

【取引 / Transaction】 得意先に商品50,000円を掛けで販売した。

Sold goods worth ¥50,000 to a customer on credit.

- (借方)現金 50,000 / (貸方)売上 50,000

Debit: Cash 50,000 / Credit: Sales 50,000 - (借方)売掛金 50,000 / (貸方)売上 50,000

Debit: Accounts Receivable 50,000 / Credit: Sales 50,000 - (借方)売上 50,000 / (貸方)売掛金 50,000

Debit: Sales 50,000 / Credit: Accounts Receivable 50,000 - (借方)仕入 50,000 / (貸方)買掛金 50,000

Debit: Purchases 50,000 / Credit: Accounts Payable 50,000

解答:2 / Answer: 2

「掛けで販売した」とは、代金を後日受け取る約束で商品を売ったことを意味します。この取引では、①売掛金(資産)が50,000円増加した、②売上(収益)が50,000円発生した、の2つが起きています。資産の増加は借方、収益の発生は貸方のルールに従い、「借方:売掛金 50,000 / 貸方:売上 50,000」が正解です。選択肢1は現金で受け取った場合の仕訳です。選択肢3は借方・貸方が逆になっています。選択肢4は仕入の仕訳であり、販売取引ではありません。

“Sold on credit” means goods were sold with the payment to be received at a later date. This transaction involves: ① Accounts Receivable (Asset) increased by ¥50,000, and ② Sales (Revenue) of ¥50,000 occurred. Following the rules — assets increase on the debit side, revenue occurs on the credit side — the correct entry is “Debit: Accounts Receivable 50,000 / Credit: Sales 50,000.” Option 1 is the entry for a cash sale. Option 3 has the debit and credit sides reversed. Option 4 is a purchase entry, not a sale.

第3問 Question 3

次の勘定科目を「資産・負債・純資産・収益・費用」の5つのグループに正しく分類したものとして、適切なものはどれか。

Which of the following correctly classifies the account titles below into the five groups of “assets, liabilities, equity, revenue, and expenses”?

【勘定科目 / Account Titles】 受取利息、買掛金、消耗品費、建物

Interest Received, Accounts Payable, Supplies Expense, Building

- 受取利息=費用、買掛金=負債、消耗品費=費用、建物=資産

Interest Received = Expense, Accounts Payable = Liability, Supplies Expense = Expense, Building = Asset - 受取利息=収益、買掛金=資産、消耗品費=費用、建物=資産

Interest Received = Revenue, Accounts Payable = Asset, Supplies Expense = Expense, Building = Asset - 受取利息=収益、買掛金=負債、消耗品費=費用、建物=資産

Interest Received = Revenue, Accounts Payable = Liability, Supplies Expense = Expense, Building = Asset - 受取利息=収益、買掛金=負債、消耗品費=資産、建物=費用

Interest Received = Revenue, Accounts Payable = Liability, Supplies Expense = Asset, Building = Expense

解答:3 / Answer: 3

受取利息は企業が受け取る利息であり「収益」です。買掛金は商品を掛けで仕入れたときに生じる支払義務であり「負債」です。消耗品費はボールペン・コピー用紙などの消耗品を購入した際の費用であり「費用」です。建物は企業が所有する不動産であり「資産」です。選択肢1は受取利息を「費用」と誤って分類しています。選択肢2は買掛金を「資産」と誤って分類しています。選択肢4は消耗品費を「資産」、建物を「費用」と誤って分類しています。

Interest Received is interest earned by the business — it is “revenue.” Accounts Payable is a payment obligation arising when goods are purchased on credit — it is a “liability.” Supplies Expense is the cost of purchasing consumable items such as pens and copy paper — it is an “expense.” Building is real property owned by the business — it is an “asset.” Option 1 incorrectly classifies Interest Received as an “expense.” Option 2 incorrectly classifies Accounts Payable as an “asset.” Option 4 incorrectly classifies Supplies Expense as an “asset” and Building as an “expense.”

- ITパスポート試験|情報セキュリティの基礎知識と対策 IT Passport Exam | Information Security: Fundamentals and Security Measures

- 日商簿記3級|現金の基礎知識と仕訳 Nissho Bookkeeping Level 3 | Cash: Fundamentals and Journal Entries

この記事を書いた人

関連記事

-

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained -

日商簿記検定3級|貸付金・借入金の仕訳と利息計算 Nissho Bookkeeping Level 3 | Loans Receivable and Loans Payable: Journal Entries and Interest Calculations

-

日商簿記3級|小口現金の仕訳 Nissho Bookkeeping Level 3 | Petty Cash Journal Entries

-

日商簿記3級|預金と当座借越の仕訳 Nissho Bookkeeping Level 3 | Deposits and Bank Overdraft Journal Entries

-

日商簿記3級|現金の基礎知識と仕訳 Nissho Bookkeeping Level 3 | Cash: Fundamentals and Journal Entries