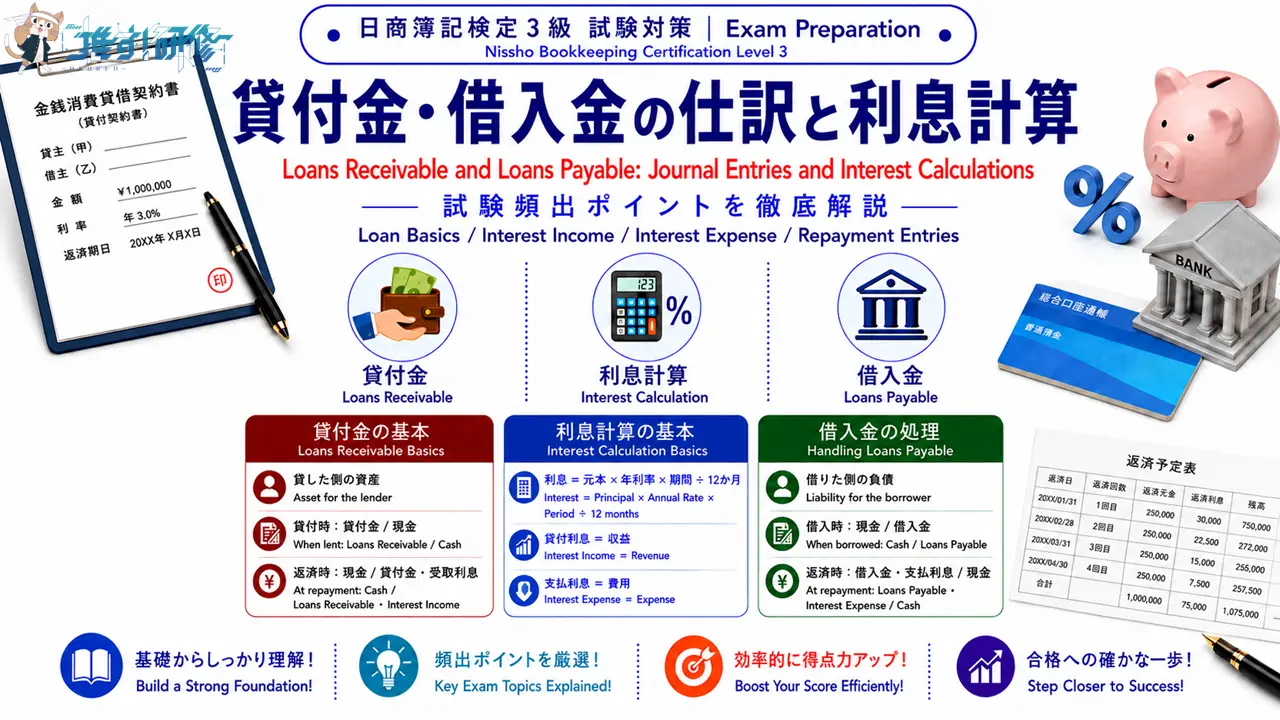

日商簿記検定3級|貸付金・借入金の仕訳と利息計算 Nissho Bookkeeping Level 3 | Loans Receivable and Loans Payable: Journal Entries and Interest Calculations

日商簿記検定3級で確実に得点したいテーマの一つが「貸付金・借入金」です。お金を貸したときと借りたとき、そして返済を受けたときと返済をしたときのそれぞれで、どの勘定科目をどちら側に記録するかを正確に理解することが、この分野の得点力を高める鍵となります。特に「利息の計算方法」と「利息にかかる勘定科目(受取利息・支払利息)の使い分け」は試験で繰り返し問われる頻出論点です。本記事では、貸付金・借入金の基本的な考え方から、利息の計算・仕訳まで、試験対策に直結するポイントを体系的に解説します。

One of the topics where you can reliably pick up marks on the Nissho Bookkeeping Level 3 exam is “loans receivable and loans payable.” The key to performing well in this area is a solid understanding of which account goes on which side of the journal entry — when lending money, when borrowing money, when receiving repayment, and when making repayment. Two points are tested particularly often: how to calculate interest, and how to distinguish between the interest income and interest expense accounts. This article provides a systematic explanation of the key exam points, from the fundamental concepts of loans receivable and loans payable through to interest calculations and journal entries.

この記事で学べること:貸付金・借入金の定義と勘定科目の分類・お金を貸し付けたときの仕訳・貸付金を返してもらったときの仕訳(受取利息の計算を含む)・お金を借り入れたときの仕訳・借入金を返したときの仕訳(支払利息の計算を含む)。出題範囲に含まれる重要ポイントを中心に整理しています。

What you’ll learn in this article: the definitions of loans receivable and loans payable and their account classifications; the journal entry when money is lent; the journal entry when repayment of a loan is received, including interest income calculations; the journal entry when money is borrowed; and the journal entry when a borrowed loan is repaid, including interest expense calculations. This article focuses on important points included in the exam scope.

目次

貸付金・借入金の基本 Loans Receivable and Loans Payable: The Basics

企業が取引先や関係会社などに対してお金を貸し付けることがあります。このとき、あとでお金を返してもらえる権利が発生します。この権利を貸付金(資産)として処理します。反対に、企業が銀行などからお金を借り入れたとき、あとでお金を返さなければならない義務が発生します。この義務を借入金(負債)として処理します。

A company sometimes lends money to business partners or related companies. When this happens, a right to receive repayment in the future arises. This right is recorded as loans receivable (asset). Conversely, when a company borrows money from a bank or other lender, an obligation to repay the money in the future arises. This obligation is recorded as loans payable (liability).

| 勘定科目 / Account | 分類 / Classification | 発生する場面 / When It Arises |

|---|---|---|

| 貸付金 Loans Receivable | 資産 / Asset | 他者にお金を貸し付けたとき When money is lent to another party |

| 借入金 Loans Payable | 負債 / Liability | 他者からお金を借り入れたとき When money is borrowed from another party |

| 受取利息 Interest Income | 収益 / Revenue | 貸し付けたお金に対する利息を受け取ったとき When interest is received on money lent |

| 支払利息 Interest Expense | 費用 / Expense | 借り入れたお金に対する利息を支払ったとき When interest is paid on money borrowed |

貸付金は資産の勘定科目であるため、増えたら借方(左)、減ったら貸方(右)に記録します。借入金は負債の勘定科目であるため、増えたら貸方(右)、減ったら借方(左)に記録します。

Since loans receivable is an asset account, it is recorded on the debit (left) side when it increases and on the credit (right) side when it decreases. Since loans payable is a liability account, it is recorded on the credit (right) side when it increases and on the debit (left) side when it decreases.

従業員・役員への貸付金 Loans to Employees and Directors

貸付金には、貸付先によって異なる勘定科目名が用いられることがあります。従業員に対する貸付金は従業員貸付金(資産)、取締役などの役員に対する貸付金は役員貸付金(資産)として処理する場合があります。試験では「貸付金」として出題されることが多いですが、こうした細分化された勘定科目名も押さえておきましょう。

The name of the loans receivable account may vary depending on who the money is lent to. Loans to employees may be recorded as employee loans receivable (asset), while loans to directors and executives may be recorded as director loans receivable (asset). Exam questions most commonly use the general term “loans receivable,” but it is worth noting these more specific account names as well.

貸付金の仕訳 Journal Entries for Loans Receivable

①お金を貸し付けたときの仕訳 Journal Entry When Money Is Lent

他社にお金を貸し付けたとき、あとで返してもらえる権利(貸付金)が発生するため、貸付金(資産)が増加します。同時に現金が出ていくため、現金(資産)が減少します。

When money is lent to another company, the right to receive repayment in the future arises, so loans receivable (asset) increases. At the same time, cash goes out, so cash (asset) decreases.

例 / Example 北陸商事は、南海物産に現金500円を貸し付けた。

Hokuriku Shoji lent ¥500 in cash to Nankai Bussan.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 貸付金(資産)500 Loans Receivable (Asset) ¥500 | 現金(資産)500 Cash (Asset) ¥500 |

②貸付金を返してもらったときの仕訳(利息を含む) Journal Entry When Repayment of a Loan Is Received (Including Interest)

貸し付けたお金が返済されたとき、返してもらう権利がなくなるため貸付金(資産)が減少します。また、貸付期間に応じた利息を受け取ります。この利息は受取利息(収益)として処理します。返済額(元本+利息)の合計が現金で入ってくるため、現金(資産)が増加します。

When the lent money is repaid, the right to receive repayment disappears, so loans receivable (asset) decreases. Interest for the lending period is also received, and this is recorded as interest income (revenue). Since the total repayment amount (principal + interest) is received in cash, cash (asset) increases.

利息の計算式 Interest Calculation Formula

貸付期間や借入期間が月数で与えられている場合、利息は次の計算式で求めます。

When the lending or borrowing period is given in months, interest is calculated using the following formula.

利息 = 貸付(借入)金額 × 年利率 × 貸付(借入)期間 ÷ 12か月

Interest = Principal × Annual Interest Rate × Lending (Borrowing) Period ÷ 12 months

例 / Example 北陸商事は、南海物産から貸付金500円の返済を受け、貸付期間6か月・年利率4%の利息とともに現金で受け取った。

Hokuriku Shoji received repayment of ¥500 in loans receivable from Nankai Bussan, along with interest calculated at an annual rate of 4% for a 6-month lending period, all received in cash.

受取利息の計算 / Interest income calculation:500円 × 4% × 6か月 ÷ 12か月 = 10円

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 現金(資産)510 Cash (Asset) ¥510 | 貸付金(資産)500 Loans Receivable (Asset) ¥500 |

| 受取利息(収益)10 Interest Income (Revenue) ¥10 |

現金の受取額は元本500円+利息10円=510円です。貸方には貸付金の減少500円と収益の発生(受取利息)10円を分けて記録します。

The total cash received is ¥500 (principal) + ¥10 (interest) = ¥510. On the credit side, the decrease in loans receivable (¥500) and the arising of revenue — interest income (¥10) — are recorded separately.

借入金の仕訳 Journal Entries for Loans Payable

③お金を借り入れたときの仕訳 Journal Entry When Money Is Borrowed

銀行などからお金を借り入れたとき、あとで返さなければならない義務(借入金)が発生するため、借入金(負債)が増加します。同時に現金が入ってくるため、現金(資産)が増加します。

When money is borrowed from a bank or other lender, an obligation to repay in the future arises, so loans payable (liability) increases. At the same time, cash is received, so cash (asset) increases.

例 / Example 東西銀行から現金2,000円を借り入れた。

¥2,000 was borrowed in cash from Tozai Bank.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 現金(資産)2,000 Cash (Asset) ¥2,000 | 借入金(負債)2,000 Loans Payable (Liability) ¥2,000 |

④借入金を返したときの仕訳(利息を含む) Journal Entry When a Borrowed Loan Is Repaid (Including Interest)

借り入れたお金を返済したとき、返さなければならない義務がなくなるため借入金(負債)が減少します。また、借入期間に応じた利息を支払います。この利息は支払利息(費用)として処理します。返済額(元本+利息)の合計が現金で出ていくため、現金(資産)が減少します。

When the borrowed money is repaid, the obligation to repay disappears, so loans payable (liability) decreases. Interest for the borrowing period is also paid, and this is recorded as interest expense (expense). Since the total repayment amount (principal + interest) goes out in cash, cash (asset) decreases.

例 / Example 東西銀行に借入金2,000円を返済し、借入期間9か月・年利率2%の利息とともに現金で支払った。

¥2,000 in loans payable was repaid to Tozai Bank, along with interest calculated at an annual rate of 2% for a 9-month borrowing period, all paid in cash.

支払利息の計算 / Interest expense calculation:2,000円 × 2% × 9か月 ÷ 12か月 = 30円

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 借入金(負債)2,000 Loans Payable (Liability) ¥2,000 | 現金(資産)2,030 Cash (Asset) ¥2,030 |

| 支払利息(費用)30 Interest Expense (Expense) ¥30 |

現金の支払額は元本2,000円+利息30円=2,030円です。借方には借入金の減少2,000円と費用の発生(支払利息)30円を分けて記録します。

The total cash paid is ¥2,000 (principal) + ¥30 (interest) = ¥2,030. On the debit side, the decrease in loans payable (¥2,000) and the arising of expense — interest expense (¥30) — are recorded separately.

貸付金と借入金の仕訳まとめ Summary of Journal Entries

4つの場面をまとめて確認しましょう。

Let’s review all four scenarios together.

| 場面 / Scenario | 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|---|

| ①貸し付けたとき When money is lent | 貸付金(資産)↑ Loans Receivable ↑ | 現金(資産)↓ Cash ↓ |

| ②貸付金を返してもらったとき When repayment of a loan is received | 現金(資産)↑ Cash ↑ | 貸付金(資産)↓ Loans Receivable ↓ 受取利息(収益)↑ Interest Income ↑ |

| ③借り入れたとき When money is borrowed | 現金(資産)↑ Cash ↑ | 借入金(負債)↑ Loans Payable ↑ |

| ④借入金を返したとき When a borrowed loan is repaid | 借入金(負債)↓ Loans Payable ↓ 支払利息(費用)↑ Interest Expense ↑ | 現金(資産)↓ Cash ↓ |

試験直前チェック Key Points to Remember

貸付金・借入金の重要ポイントをまとめます。

Here is a summary of the key points on loans receivable and loans payable.

- 貸付金は資産・借入金は負債 貸付金は「返してもらえる権利」なので資産、借入金は「返さなければならない義務」なので負債

Loans receivable is an asset; loans payable is a liability — loans receivable is an asset because it represents the right to receive repayment; loans payable is a liability because it represents the obligation to repay - 利息の勘定科目を区別する 貸し付けた側が受け取る利息は受取利息(収益)、借り入れた側が支払う利息は支払利息(費用)

Distinguish between interest accounts — interest received by the lender is interest income (revenue); interest paid by the borrower is interest expense (expense) - 利息の計算は期間の単位に注意する 期間が月数で与えられている場合は、利息=元本×年利率×期間÷12か月で月割り計算を行う。期間が日数で与えられている場合は、問題文の指示に従って日割り計算を行う

Pay attention to the time unit in interest calculations — When the period is given in months, use Interest = Principal × Annual Rate × Period ÷ 12 months. When the period is given in days, calculate on a daily basis according to the instructions in the question - 返済時は元本と利息を分けて記録する 返済を受けたとき・返済をしたときのいずれも、元本と利息は別々の勘定科目で記録する

Record principal and interest separately at repayment — whether receiving or making repayment, the principal and interest are always recorded using separate accounts - 現金の受払額=元本+利息 返済時に動く現金の合計額は「元本+利息」であることを確認してから仕訳を組む

Cash received/paid = principal + interest — always confirm that the total cash amount at repayment equals principal plus interest before recording the journal entry

なお、貸付期間や借入期間が決算日をまたぐ場合には、当期分の利息を決算整理で見越し計上することがあります(未収利息・未払利息)。まずは本記事のように「返済時に元本と利息を分けて処理する」基本形を確実に押さえたうえで、決算整理の学習へと進みましょう。

Note that when a lending or borrowing period straddles the balance sheet date, interest accrued for the current period may need to be recognized through adjusting entries at year-end (as accrued interest receivable or accrued interest payable). Be sure to first master the fundamental approach covered in this article — recording principal and interest separately at repayment — before moving on to year-end adjusting entries.

練習問題で理解を確認しよう Practice Questions

ここまでの内容を試験形式で確認しましょう。解答と解説は各問題の直下に記載しています。

Let’s check your understanding with some exam-style practice questions. The answer and explanation for each question appear directly below it.

第1問 Question 1

次の一連の取引について仕訳しなさい。

Record the journal entries for the following series of transactions.

- さくら商事は、みどり産業に現金800円を、貸付期間6か月・年利率3%の条件で貸し付けた。なお、利息は返済時に受け取る。

Sakura Trading lent ¥800 in cash to Midori Industries for a period of 6 months at an annual interest rate of 3%. Interest is to be received at the time of repayment. - さくら商事はみどり産業より(1)の貸付金の返済を受け、利息とともに現金で受け取った。

Sakura Trading received repayment of the loan in (1) from Midori Industries, along with interest, all in cash.

解答 / Answer

受取利息の計算 / Interest income calculation:800円 × 3% × 6か月 ÷ 12か月 = 12円

| 借方(左)/ Debit | 貸方(右)/ Credit | |

|---|---|---|

| (1) | 貸付金(資産)800 Loans Receivable (Asset) ¥800 | 現金(資産)800 Cash (Asset) ¥800 |

| (2) | 現金(資産)812 Cash (Asset) ¥812 | 貸付金(資産)800 Loans Receivable (Asset) ¥800 受取利息(収益)12 Interest Income (Revenue) ¥12 |

(1)他社にお金を貸し付けると、あとで返してもらえる権利が生まれるため、貸付金(資産)が800円増加します。同時に現金が出ていくため、現金(資産)が800円減少します。(2)貸付金が返済されると、返してもらえる権利がなくなるため、貸付金(資産)が800円減少します。また、利息800円×3%×6÷12=12円を受け取るため、受取利息(収益)が12円発生します。現金の受取額は元本800円+利息12円=812円となります。

(1) Sakura Trading lends money to Midori Industries, creating the right to receive repayment, so loans receivable (asset) increases by ¥800. Cash goes out at the same time, so cash (asset) decreases by ¥800. (2) When the loan is repaid, the right to receive repayment disappears, so loans receivable (asset) decreases by ¥800. Interest of ¥800 × 3% × 6 ÷ 12 = ¥12 is also received, giving rise to interest income (revenue) of ¥12. The total cash received is ¥800 (principal) + ¥12 (interest) = ¥812.

第2問 Question 2

次の一連の取引について仕訳しなさい。

Record the journal entries for the following series of transactions.

- あさひ商事は、つばき銀行より現金4,000円を、借入期間8か月・年利率3%の条件で借り入れた。なお、利息は返済時に支払う。

Asahi Commerce borrowed ¥4,000 in cash from Tsubaki Bank for a period of 8 months at an annual interest rate of 3%. Interest is to be paid at the time of repayment. - あさひ商事はつばき銀行に(1)の借入金を返済し、利息とともに現金で支払った。

Asahi Commerce repaid the loan in (1) to Tsubaki Bank, along with interest, all in cash.

解答 / Answer

支払利息の計算 / Interest expense calculation:4,000円 × 3% × 8か月 ÷ 12か月 = 80円

| 借方(左)/ Debit | 貸方(右)/ Credit | |

|---|---|---|

| (1) | 現金(資産)4,000 Cash (Asset) ¥4,000 | 借入金(負債)4,000 Loans Payable (Liability) ¥4,000 |

| (2) | 借入金(負債)4,000 Loans Payable (Liability) ¥4,000 支払利息(費用)80 Interest Expense (Expense) ¥80 | 現金(資産)4,080 Cash (Asset) ¥4,080 |

(1)銀行からお金を借り入れると、あとで返さなければならない義務が生まれるため、借入金(負債)が4,000円増加します。同時に現金が入ってくるため、現金(資産)が4,000円増加します。(2)借入金を返済すると、返さなければならない義務がなくなるため、借入金(負債)が4,000円減少します。また、利息4,000円×3%×8÷12=80円を支払うため、支払利息(費用)が80円発生します。現金の支払額は元本4,000円+利息80円=4,080円となります。

(1) Asahi Commerce borrows money from Tsubaki Bank, creating an obligation to repay in the future, so loans payable (liability) increases by ¥4,000. Cash is received at the same time, so cash (asset) increases by ¥4,000. (2) When the loan is repaid, the obligation to repay disappears, so loans payable (liability) decreases by ¥4,000. Interest of ¥4,000 × 3% × 8 ÷ 12 = ¥80 is also paid, giving rise to interest expense (expense) of ¥80. The total cash paid is ¥4,000 (principal) + ¥80 (interest) = ¥4,080.

第3問 Question 3

貸付金・借入金に関する次の記述のうち、誤っているものはどれか。

Which of the following statements about loans receivable and loans payable is incorrect?

- ア 他社にお金を貸し付けたとき、貸付金(資産)が増加する。

When money is lent to another company, loans receivable (asset) increases. - イ 借り入れたお金を返済したとき、支払う利息は受取利息(収益)として処理する。

When borrowed money is repaid, the interest paid is recorded as interest income (revenue). - ウ 貸付金の返済を受けたとき、現金の受取額は元本と利息の合計になる。

When repayment of a loan is received, the total cash received equals the sum of the principal and interest. - エ 利息の計算は「元本×年利率×期間÷12か月」の式で月割り計算を行う。

Interest is calculated using the formula “Principal × Annual Rate × Period ÷ 12 months” on a monthly pro-rata basis.

解答:イ / Answer: イ

選択肢イが誤りです。借り入れたお金を返済したときに支払う利息は、支払利息(費用)として処理します。受取利息(収益)は、お金を貸し付けた側(貸付金を持つ側)が利息を受け取ったときに使う勘定科目です。借り入れた側(借入金を持つ側)が利息を支払うときは必ず支払利息を使います。選択肢ア・ウ・エはいずれも正しい記述です。

Option イ is incorrect. When borrowed money is repaid, the interest paid is recorded as interest expense (expense) — not interest income (revenue). Interest income is used when the lender (the party holding loans receivable) receives interest. The borrower (the party holding loans payable) always uses interest expense when paying interest. Options ア, ウ, and エ are all correct statements.

- ITパスポート試験|プロジェクトマネジメントの基礎知識と計算問題 IT Passport Exam | Project Management: Fundamentals and Calculation Problems

- 森鷗外『最後の一句』に学ぶ——職場で「言うべきことを言える人」を育てる文学研修 Learning from Mori Ōgai's Saigo no Ikku: A Literary Approach to Developing People Who Speak Up at Work

この記事を書いた人

関連記事

-

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained -

日商簿記3級|小口現金の仕訳 Nissho Bookkeeping Level 3 | Petty Cash Journal Entries

-

日商簿記3級|預金と当座借越の仕訳 Nissho Bookkeeping Level 3 | Deposits and Bank Overdraft Journal Entries

-

日商簿記3級|現金の基礎知識と仕訳 Nissho Bookkeeping Level 3 | Cash: Fundamentals and Journal Entries

-

日商簿記3級|仕訳の基礎知識と借方・貸方のルール Nissho Bookkeeping Level 3 | Journal Entries: Fundamentals and Debit and Credit Rules