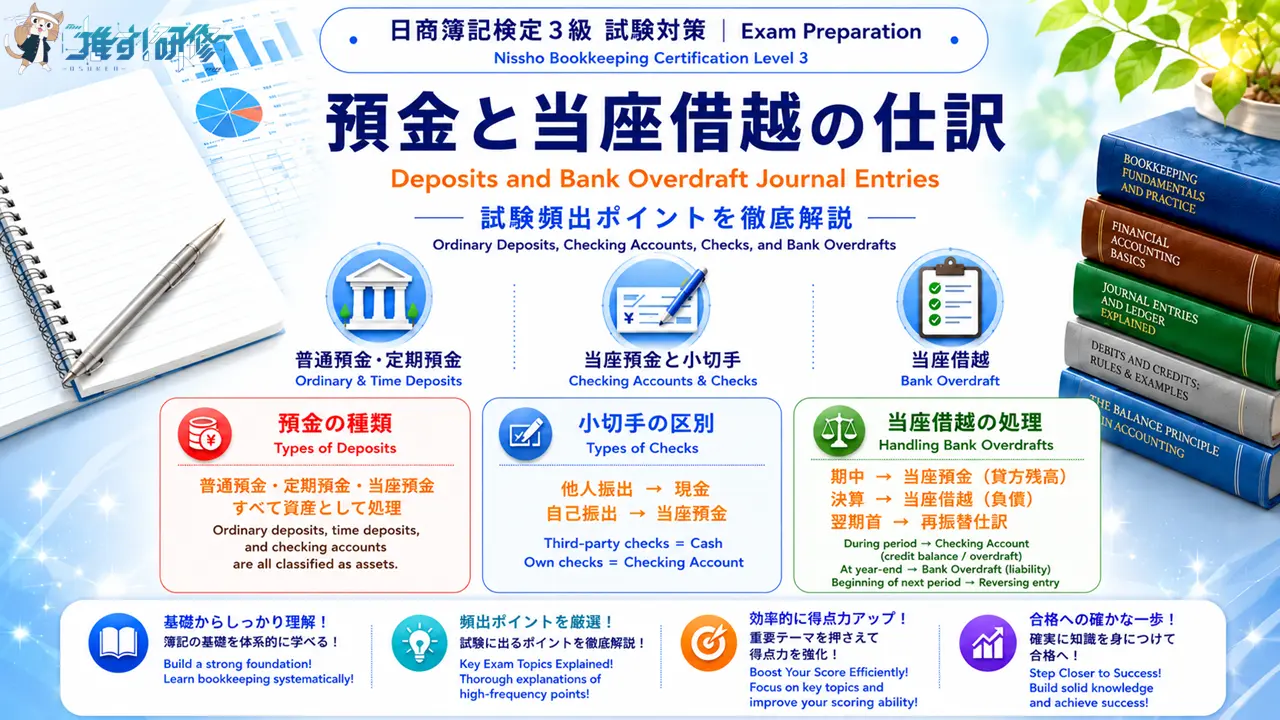

日商簿記3級|預金と当座借越の仕訳 Nissho Bookkeeping Level 3 | Deposits and Bank Overdraft Journal Entries

日商簿記検定3級で必ず出題されるテーマの一つが「預金」です。普通預金・定期預金・当座預金の3種類の預金と、当座借越の処理を正確に理解することが、この分野で確実に得点するための鍵です。特に「小切手を誰が振り出したか」によって処理が変わる点と、決算時の当座借越の振り替えは試験頻出の論点です。本記事では、各預金の仕訳から当座借越の決算処理まで、試験に直結するポイントを体系的に解説します。

Bank deposits are one of the frequently tested topics on the Nissho Bookkeeping Level 3 exam. Mastering the three types of deposits — ordinary deposits, time deposits, and checking accounts — along with the handling of bank overdrafts is essential for scoring well on this topic. Two points in particular require careful attention: how the journal entry changes depending on who issued the check, and how bank overdrafts are treated at year-end. This article provides a systematic explanation of the key exam points, from the journal entries for each deposit type to the year-end treatment of bank overdrafts.

この記事で学べること:普通預金・定期預金・当座預金それぞれの仕訳・小切手の振出と自己振出小切手の処理・当座借越の仕訳と決算時の振替・再振替仕訳。すべて試験に出るポイントに絞っています。

What you’ll learn in this article: journal entries for ordinary deposits, time deposits, and checking accounts; the treatment of issued checks and checks drawn by your own company; bank overdraft journal entries and the year-end reclassification; and the reversing entry at the start of the next period. Every point is selected specifically because it appears on the exam.

目次

普通預金と定期預金の基本 Ordinary Deposits and Time Deposits: The Basics

普通預金と定期預金はどちらも資産として分類されます。現金を預け入れると、現金(資産)が減少し、各預金勘定(資産)が増加します。

Both ordinary deposits and time deposits are classified as assets. When cash is deposited, cash (an asset) decreases and the corresponding deposit account (an asset) increases.

普通預金への預け入れ Depositing Cash into an Ordinary Account

現金を普通預金口座に預け入れたときは、普通預金(資産)が増加し、現金(資産)が減少します。

When cash is deposited into an ordinary account, ordinary deposit (asset) increases and cash (asset) decreases.

例 / Example 現金200円を南北銀行の普通預金口座に預け入れた。

¥200 in cash was deposited into an ordinary bank account at Nanboku Bank.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 普通預金(資産)200 Ordinary Deposit (Asset) ¥200 | 現金(資産)200 Cash (Asset) ¥200 |

定期預金への預け替え Transferring Funds to a Time Deposit Account

定期預金は預金の一種で、原則として満期時のみ引き出しが可能です(預け入れはいつでも行えます)。普通預金口座から定期預金口座へ資金を移した場合、普通預金(資産)が減少し、定期預金(資産)が増加します。

A time deposit is a type of deposit in which withdrawals are generally only permitted at maturity (deposits can generally be made at any time). When funds are moved from an ordinary account to a time deposit account, the ordinary deposit (asset) decreases and the time deposit (asset) increases.

例 / Example 南北銀行の普通預金口座から定期預金口座へ500円を預け替えた。

¥500 was transferred from an ordinary deposit account to a time deposit account at Nanboku Bank.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 定期預金(資産)500 Time Deposit (Asset) ¥500 | 普通預金(資産)500 Ordinary Deposit (Asset) ¥500 |

当座預金と小切手の仕組み How Checking Accounts and Checks Work

当座預金は預金の一種ですが、普通預金と異なり利息がつかない代わりに、小切手を使って預金を引き出すことができます。商取引での代金支払いに広く活用される預金口座です。

A checking account is a type of deposit that, unlike an ordinary deposit, does not earn interest, but allows withdrawals by using checks. It is widely used as a means of payment in commercial transactions.

当座預金への預け入れ Depositing Cash into a Checking Account

現金を当座預金口座に預け入れたときは、当座預金(資産)が増加し、現金(資産)が減少します。

When cash is deposited into a checking account, checking account (asset) increases and cash (asset) decreases.

例 / Example 南北銀行と当座取引契約を結び、現金400円を当座預金口座に預け入れた。

After opening a checking account at Nanboku Bank, ¥400 in cash was deposited.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 当座預金(資産)400 Checking Account (Asset) ¥400 | 現金(資産)400 Cash (Asset) ¥400 |

小切手を振り出して支払う Making Payment by Issuing a Check

小切手を振り出して代金を支払ったときは、当座預金(資産)が減少します。小切手を受け取った相手が銀行に持ち込むことで、振出人の当座預金口座から資金が引き出されるためです。

When a check is issued as payment, the checking account (asset) decreases. This is because when the recipient presents the check at a bank, funds are withdrawn from the issuer’s checking account.

例 / Example 白川商事に対する買掛金300円を支払うため、小切手を振り出して渡した。

A check for ¥300 was issued and handed over to Shirakawa Trading Co. to settle an accounts payable balance.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 買掛金(負債)300 Accounts Payable (Liability) ¥300 | 当座預金(資産)300 Checking Account (Asset) ¥300 |

振出人で変わる小切手の処理 Check Treatment: Your Own Company vs. Another Party

小切手の仕訳で最も注意が必要なのが、「誰が振り出した小切手か」による処理の違いです。振出人が自社か他社かによって、使う勘定科目が異なります。

The most important distinction in check-related journal entries is “who issued the check.” The account used differs depending on whether the check was drawn by your own company or by another party.

| 小切手の種類 / Type of Check | 処理 / Treatment |

|---|---|

| 他人振出小切手 Check drawn by another party | 現金(資産)として処理 Treated as cash (asset) |

| 自己振出小切手 Check drawn by your own company | 当座預金(資産)の増加として処理 Treated as an increase in checking account (asset) |

自己振出小切手が手元に戻ってきたとき、現金ではなく当座預金として処理するのは、小切手を振り出した時点で当座預金を減らしていたためです。その小切手が戻ってきた場合は、減らした当座預金を元に戻す(増やす)処理を行います。

When a check issued by your own company is returned, it is recorded as an increase in the checking account rather than as cash. This is because the checking account was decreased when the check was originally issued — receiving it back simply reverses that original entry.

例 / Example 売掛金250円の回収として、以前自社が振り出した小切手を受け取った。

A check previously issued by the company itself was received as collection of ¥250 in accounts receivable.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 当座預金(資産)250 Checking Account (Asset) ¥250 | 売掛金(資産)250 Accounts Receivable (Asset) ¥250 |

当座借越の仕組みと処理 Bank Overdraft: How It Works

当座預金は残高の範囲内でしか引き出せないのが原則です。しかし、銀行と当座借越契約を事前に締結しておくことで、残高を超えた引き出しが一定の限度額まで認められます。残高を超えて引き出している状態を当座借越(とうざかりこし)といいます。

As a general rule, withdrawals from a checking account are limited to the available balance. However, when a bank overdraft agreement has been arranged in advance, withdrawals beyond the balance are permitted up to a specified limit. The state of having withdrawn more than the available balance is called a bank overdraft (当座借越).

残高を超えた引き出しの処理 Recording a Withdrawal That Exceeds the Account Balance

当座借越契約がある場合、残高を超えて小切手を振り出したときも、当座預金(資産)の減少として処理します。結果として当座預金の残高がマイナス(貸方残高)になります。

When a bank overdraft agreement is in place and a check is issued exceeding the account balance, the transaction is still recorded as a decrease in the checking account (asset), resulting in a negative (credit) balance in the checking account.

例 / Example 買掛金600円を支払うため小切手を振り出した。なお、当座預金の残高は350円であり、南北銀行と限度額500円の当座借越契約を結んでいる。

A check for ¥600 was issued to pay accounts payable. The checking account balance was ¥350, but a bank overdraft agreement with a limit of ¥500 is in place with Nanboku Bank.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 買掛金(負債)600 Accounts Payable (Liability) ¥600 | 当座預金(資産)600 Checking Account (Asset) ¥600 |

この時点での当座預金残高:350円 − 600円 = △250円(貸方残高)。限度額500円の範囲内のため、当座借越が認められます。

Checking account balance at this point: ¥350 − ¥600 = −¥250 (credit balance). Since this is within the ¥500 overdraft limit, the overdraft is permitted.

決算での当座借越への振り替え Reclassifying the Overdraft Balance at Year-End

決算日に当座預金が貸方残高(マイナスの状態)になっているということは、銀行から資金を借りている状態と同じです。資産勘定がマイナスのまま決算書に表示することはできないため、貸方残高となっている当座預金を「当座借越(負債)」または「借入金(負債)」に振り替えます。どちらを使用するかは問題文の指示に従います。

A credit balance in the checking account at year-end means the company is effectively borrowing from the bank. Since a negative balance cannot remain in an asset account on the financial statements, the credit balance is reclassified to “Bank Overdraft” (liability) or “Loans Payable” (liability). Which account to use is determined by the instructions in the exam question.

例 / Example 3月31日(決算日)において当座預金が250円の貸方残高であるため、当座借越に振り替える。

On March 31 (the closing date), the checking account has a credit balance of ¥250 and is to be reclassified to Bank Overdraft.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 当座預金(資産)250 Checking Account (Asset) ¥250 | 当座借越(負債)250 Bank Overdraft (Liability) ¥250 |

翌期首の再振替仕訳とは Understanding the Reversing Entry at Period Start

決算日に当座借越(または借入金)へ振り替えた場合、翌会計期間の最初の日(翌期首)に、決算日の仕訳の逆仕訳を行います。この仕訳を再振替仕訳(さいふりかえしわけ)といい、当座預金口座の処理を期中の通常の状態へ戻す役割を果たします。

When the checking account balance was reclassified to Bank Overdraft (or Loans Payable) at year-end, the reverse of that entry is recorded on the first day of the next accounting period. This is called a reversing entry (再振替仕訳) and serves to restore the checking account to its normal operating state for the new period.

例 / Example 翌期首において、前期決算日に行った当座借越への振替仕訳を逆仕訳する。

At the start of the next period, the year-end reclassification entry is reversed.

| 借方(左)/ Debit | 貸方(右)/ Credit |

|---|---|

| 当座借越(負債)250 Bank Overdraft (Liability) ¥250 | 当座預金(資産)250 Checking Account (Asset) ¥250 |

試験直前チェック Key Points to Remember

預金と当座借越の重要ポイントをまとめます。

Here is a summary of the key points on deposits and bank overdrafts.

- 普通預金・定期預金・当座預金はすべて資産 現金を預け入れると現金(資産)が減り、各預金(資産)が増える

Ordinary deposits, time deposits, and checking accounts are all assets — depositing cash decreases cash (asset) and increases the relevant deposit account (asset) - 定期預金の特徴 原則として満期時のみ引き出し可能。普通預金からの振替は(定期預金)/(普通預金)

Time deposit characteristics — Withdrawals are generally only permitted at maturity. Transfer from ordinary account: Debit: Time Deposit / Credit: Ordinary Deposit - 当座預金の特徴 利息なし・小切手で引き出す。小切手振出時は当座預金(資産)の減少

Checking account characteristics — No interest; withdrawals by check. Issuing a check decreases the checking account (asset) - 小切手の処理は振出人で決まる 他人振出小切手→現金、自己振出小切手→当座預金の増加

Check treatment depends on who issued it — Check drawn by another party → cash; check drawn by own company → increase in checking account - 当座借越の決算処理 決算日に当座預金が貸方残高→当座借越(負債)または借入金(負債)に振り替え。翌期首に再振替仕訳(逆仕訳)を行う

Year-end treatment of bank overdraft — Credit balance in checking account at year-end → reclassify to Bank Overdraft (liability) or Loans Payable (liability). Record the reversing entry at the start of the next period

練習問題で理解を確認しよう Practice Questions

ここまでの内容を試験形式で確認しましょう。解答と解説は各問題の直下に記載しています。

Let’s check your understanding with some exam-style practice questions. The answer and explanation for each question appear directly below it.

第1問 Question 1

次の取引の仕訳として、適切なものはどれか。

Which of the following is the correct journal entry for the transaction below?

【取引 / Transaction】 得意先である緑川物産から売掛金350円を回収した。なお、受け取ったのは同社が振り出した小切手であった。

¥350 in accounts receivable was collected from Midorikawa Bussan (a customer). The payment received was a check drawn by the customer.

- (借方)当座預金 350 / (貸方)売掛金 350

Debit: Checking Account 350 / Credit: Accounts Receivable 350 - (借方)現金 350 / (貸方)売掛金 350

Debit: Cash 350 / Credit: Accounts Receivable 350 - (借方)売掛金 350 / (貸方)現金 350

Debit: Accounts Receivable 350 / Credit: Cash 350 - (借方)普通預金 350 / (貸方)売掛金 350

Debit: Ordinary Deposit 350 / Credit: Accounts Receivable 350

解答:2 / Answer: 2

得意先(他人)が振り出した小切手を受け取った場合、その小切手は簿記上の現金(通貨代用証券)として扱います。したがって、借方は「現金」となります。選択肢1の当座預金は、受け取った小切手が自社の振り出した小切手(自己振出小切手)だった場合の処理であり、今回は誤りです。選択肢3は借貸が逆になっており誤りです。選択肢4の普通預金は、今回の取引と関係がありません。

When a check drawn by a customer (another party) is received, it is treated as cash in bookkeeping. The debit is therefore “Cash.” Option 1 (Checking Account) applies when the check received was issued by your own company — not when a check drawn by another party is received. Option 3 has the debit and credit reversed and is incorrect. Option 4 (Ordinary Deposit) is unrelated to this transaction.

第2問 Question 2

次の一連の取引について仕訳しなさい。

Record the journal entries for the following series of transactions.

- 南北銀行と当座取引契約を結び、現金450円を当座預金口座に預け入れた。

A checking account was opened at Nanboku Bank and ¥450 in cash was deposited. - 買掛金700円を支払うため、小切手を振り出して渡した。なお、南北銀行とは限度額600円の当座借越契約を結んでいる。

A check for ¥700 was issued to pay accounts payable. A bank overdraft agreement with a limit of ¥600 is in place with Nanboku Bank. - 本日決算日につき、当座預金の貸方残高を当座借越に振り替える。

Today is the closing date. The credit balance in the checking account is to be reclassified to Bank Overdraft.

解答 / Answer

| 借方(左)/ Debit | 貸方(右)/ Credit | |

|---|---|---|

| (1) | 当座預金(資産)450 Checking Account (Asset) ¥450 | 現金(資産)450 Cash (Asset) ¥450 |

| (2) | 買掛金(負債)700 Accounts Payable (Liability) ¥700 | 当座預金(資産)700 Checking Account (Asset) ¥700 |

| (3) | 当座預金(資産)250 Checking Account (Asset) ¥250 | 当座借越(負債)250 Bank Overdraft (Liability) ¥250 |

(1)現金450円を当座預金口座に預け入れたため、当座預金(資産)が増加し現金(資産)が減少します。(2)小切手700円を振り出したため当座預金(資産)が700円減少します。(1)で450円預け入れていたため、当座預金残高は450円-700円=△250円(貸方残高)となります。限度額600円の範囲内のため、当座借越が認められます。(3)決算日に当座預金が250円の貸方残高となっているため、この250円を当座借越(負債)に振り替えます。

(1) Depositing ¥450 into the checking account increases the checking account (asset) and decreases cash (asset). (2) Issuing a check for ¥700 decreases the checking account (asset) by ¥700. Since ¥450 was deposited in (1), the balance is ¥450 − ¥700 = −¥250 (credit balance). This is within the ¥600 overdraft limit, so the overdraft is permitted. (3) At year-end, the checking account has a credit balance of ¥250, which is reclassified to Bank Overdraft (liability).

第3問 Question 3

当座借越に関する次の記述のうち、誤っているものはどれか。

Which of the following statements about bank overdrafts is incorrect?

- 当座借越契約を結んでいれば、当座預金の残高を超えて小切手を振り出すことができる。

If a bank overdraft agreement is in place, checks can be issued exceeding the checking account balance. - 当座預金残高を超えて小切手を振り出したときは、超過分のみを当座借越(負債)として別途記録する。

When a check is issued exceeding the checking account balance, only the excess amount is separately recorded as Bank Overdraft (liability). - 決算日に当座預金が貸方残高の場合、当座借越(負債)または借入金(負債)に振り替える。

If the checking account has a credit balance at year-end, it is reclassified to Bank Overdraft (liability) or Loans Payable (liability). - 翌期首には、決算日に行った当座借越への振替仕訳の逆仕訳(再振替仕訳)を行う。

At the start of the next period, the reversing entry of the year-end reclassification is recorded.

解答:2 / Answer: 2

選択肢2が誤りです。当座預金残高を超えて小切手を振り出したとき、超過分だけを別途「当座借越」として記録するのではなく、支払金額の全額を当座預金(資産)の減少として処理します。その結果、当座預金残高がマイナス(貸方残高)になるだけです。当座借越(負債)として記録するのは、決算日に貸方残高を振り替えるときに限られます。選択肢1・3・4はすべて正しい記述です。

Option 2 is incorrect. When a check is issued exceeding the checking account balance, the entire payment amount is recorded as a decrease in the checking account (asset) — not just the excess portion separately as Bank Overdraft. The result is simply a negative (credit) balance in the checking account. Bank Overdraft (liability) is only used when the credit balance is reclassified at year-end. Options 1, 3, and 4 are all correct statements.

- QC3|管理図の考え方とX̄-R管理図の計算方法をわかりやすく解説 QC Level 3 | Control Charts and X̄-R Chart Calculations Explained

- ITパスポート試験|サービスマネジメントの基礎知識 IT Passport Exam | Service Management: Fundamentals and Key Concepts

この記事を書いた人

関連記事

-

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained

日商簿記検定3級|未払金・未収入金・前払金・前受金・仮払金・仮受金の仕訳を解説 Nissho Bookkeeping Level 3 | Six Key Receivable and Payable Accounts Explained -

日商簿記検定3級|貸付金・借入金の仕訳と利息計算 Nissho Bookkeeping Level 3 | Loans Receivable and Loans Payable: Journal Entries and Interest Calculations

-

日商簿記3級|小口現金の仕訳 Nissho Bookkeeping Level 3 | Petty Cash Journal Entries

-

日商簿記3級|現金の基礎知識と仕訳 Nissho Bookkeeping Level 3 | Cash: Fundamentals and Journal Entries

-

日商簿記3級|仕訳の基礎知識と借方・貸方のルール Nissho Bookkeeping Level 3 | Journal Entries: Fundamentals and Debit and Credit Rules